Person reviewing a car loan contract with car keys on a desk

What Is a Prepayment Penalty Car Loan

Content

Content

When you take out auto financing that includes a prepayment penalty clause, your lender will charge an additional fee if you eliminate the debt before its scheduled completion date. This contractual provision serves as compensation for the interest revenue your lender loses when you settle the obligation ahead of schedule—whether by making a single large payment, selling your car, or moving the debt to another institution.

Not every auto financing agreement contains this provision. While some financial institutions include them systematically, others apply them selectively based on creditworthiness, and a growing number have abandoned them completely to attract customers. Knowing whether this clause exists in your contract—and calculating its potential cost—could mean the difference between hundreds and thousands of dollars.

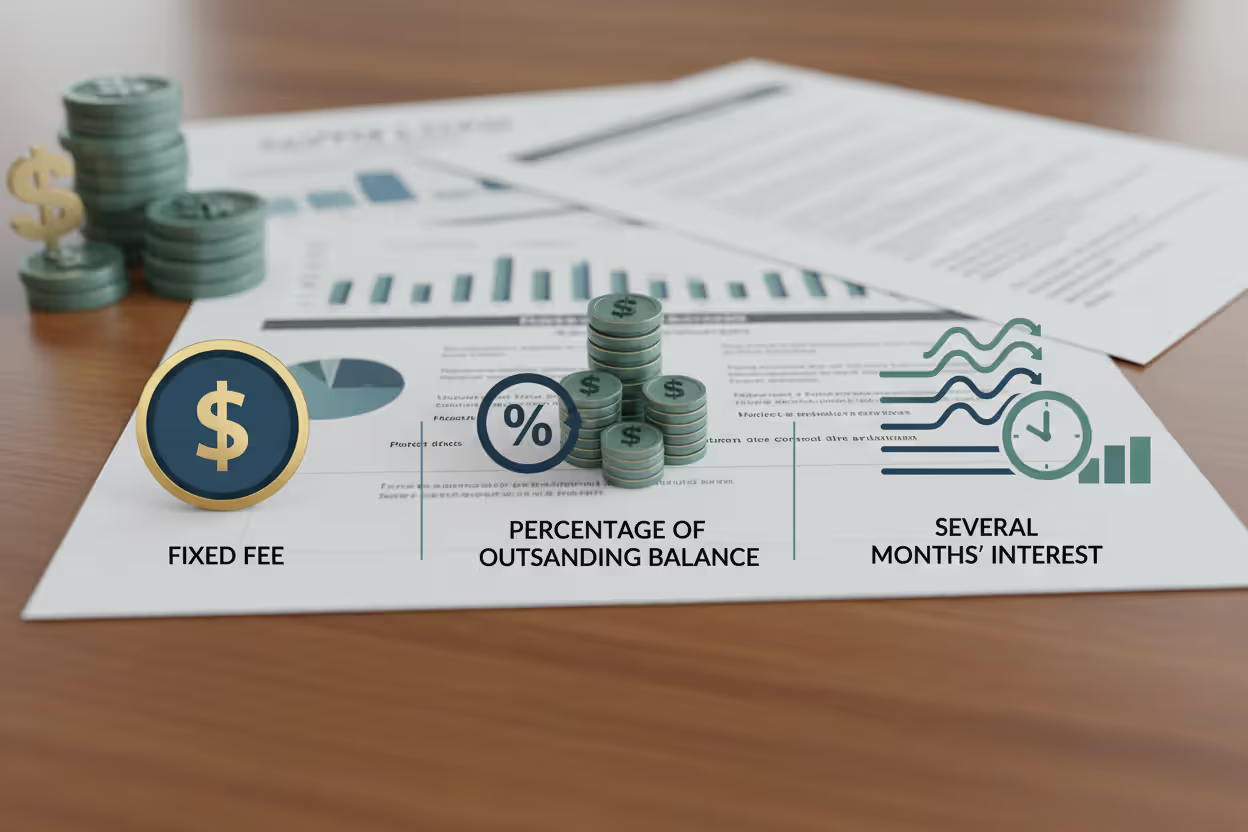

These fees come in various forms. Your contract might specify a fixed charge between $200 and $500, require a percentage of what you still owe (usually between 1% and 2%), or base the calculation on multiple months of expected interest payments. Most contracts limit these charges to the initial 12 to 36 months, allowing you to eliminate the debt without extra costs after that window closes.

How Prepayment Penalties Work on Auto Loans

Financial institutions generate revenue primarily from the interest you pay across your loan's lifespan. Eliminating a car loan ahead of schedule cuts off that income stream, particularly impacting longer-term agreements where interest represents a major component of total repayment. The auto loan prepayment fee serves as replacement income for these lost earnings.

Three main penalty formats dominate the market. Under a percentage-based structure, you'll pay 1% to 2% of what you currently owe. For instance, with $15,000 remaining and a 2% contract provision, you'd face an extra $300 charge. A fixed-amount structure might demand $150 to $500 without regard to your balance. The third category, though less widespread but potentially costlier, determines penalties by interest duration—commonly two to six months of the interest you would have otherwise paid.

Author: Brandon Ellsworth;

Source: ruralxchange.net

The timeframe during which penalties apply carries tremendous significance. Your agreement might impose charges exclusively during the initial 24 months, so settling the debt in month 25 costs nothing extra. Other contracts employ declining structures: 2% during the first year, 1% during the second, nothing afterward.

Financial institutions defend these charges because auto loan payment structures favor lenders initially. During the opening months and years, larger portions of each payment service interest obligations while smaller portions reduce your principal. When you eliminate a six-year loan during its second year, your lender has captured only a small fraction of anticipated interest despite bearing full origination and servicing expenses.

Subprime lenders incorporate prepayment penalties more consistently than institutions serving borrowers with stronger credit. Those with credit scores falling below 620 frequently encounter these provisions because lenders categorize them as higher-risk customers and require guaranteed minimum returns. The early payoff fee car loan structure helps counterbalance the increased likelihood of default these portfolios experience.

How to Check If Your Car Loan Has a Prepayment Penalty

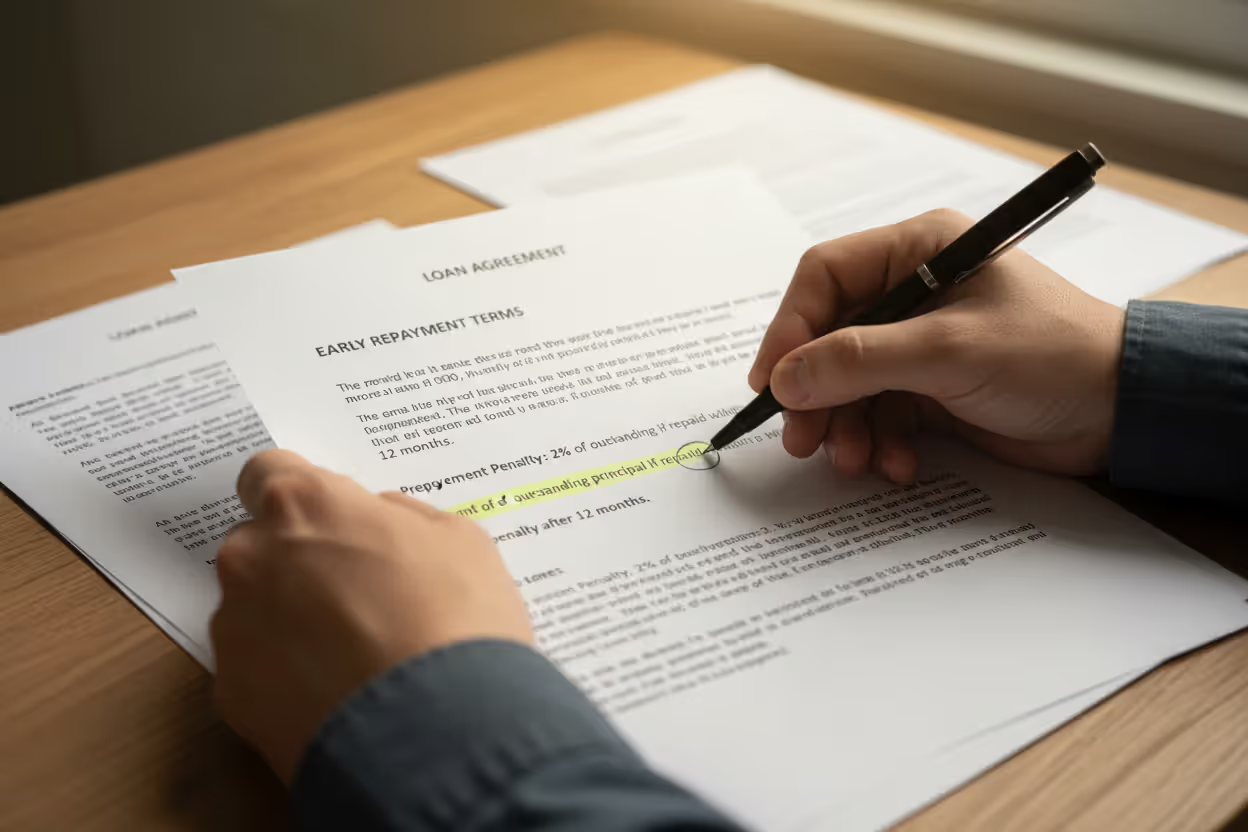

Your financing contract holds this critical information, though locating it demands thorough examination. Search for headings labeled "Prepayment," "Early Termination," or "Payoff Terms." The penalty language often appears in smaller print alongside disclosures covering late charges and default conditions.

Federal Truth in Lending Act regulations mandate that lenders reveal prepayment penalties within your loan paperwork, particularly in the standardized disclosure summary highlighting essential terms. Examine the entry for "Prepayment penalty" or "Early payoff fee." A designation of "None" or "No penalty" means you face no charges. Finding "Yes" or seeing a specific dollar figure or percentage requires investigating the corresponding contract provisions for complete details.

Contact your lender's service department and pose this direct question: "Does my financing include a prepayment penalty, and what amount would I owe for settling today's balance?" Ask for written documentation of the payoff amount. This statement displays your existing principal, accumulated interest calculated through the settlement date, and all applicable charges.

Individual state disclosure mandates differ considerably. Certain states require lenders to present prepayment penalties using bold typography or separate disclosure documentation. Others mandate verbal explanation during application processing. Federal regulations guarantee the information appears somewhere in your documentation regardless of state-specific requirements.

Examine your financing agreement within days of execution. Multiple states provide rescission windows allowing you to void specific contracts. Discovering an unanticipated penalty clause might leave you with opportunities to renegotiate or pursue different financing.

Author: Brandon Ellsworth;

Source: ruralxchange.net

States That Restrict or Ban Auto Loan Prepayment Penalties

State-level consumer protection legislation addressing car loan prepayment penalties varies widely, though coverage remains less comprehensive than mortgage-related regulations. Federal law doesn't prohibit these charges on auto financing outright, leaving primary regulatory authority with state governments.

Various states have implemented restrictions:

| State | Regulatory Approach | Specific Requirements |

| California | Selective prohibition | Banned on financing under $10,000; capped at 2% for larger amounts during initial year exclusively |

| Maryland | Transparency mandate | Requires prominent disclosure; cannot surpass 1% of outstanding principal |

| New York | Time-limited allowance | Charges permitted exclusively during opening 90-day period |

| Illinois | Declining percentage limit | Capped at 2% during first year, 1% during second year, forbidden subsequently |

| Texas | Market-based approach | No specific limitations; depends on federal disclosure standards |

| Florida | Voluntary compliance | No statutory restrictions; competitive pressure encourages lender restraint |

Legislative frameworks evolve regularly as state governments balance consumer advocacy concerns against industry arguments. Confirm current statutes in your location, as this information reflects regulations current in early 2026.

Certain states avoid restricting the charges themselves, instead establishing rigorous disclosure standards that discourage lenders from incorporating them. When borrowers receive transparent information about penalties before signing, many select competitors with more favorable conditions, generating marketplace dynamics that accomplish outcomes similar to direct prohibition.

Federal Regulations on Early Payoff Fees

The Truth in Lending Act and its implementing regulation, Regulation Z, mandate disclosure without prohibiting prepayment penalties on auto financing. This regulatory approach differs dramatically from certain mortgage categories where federal law either bans or substantially restricts such charges.

The Consumer Financial Protection Bureau oversees auto lending operations but hasn't published specific regulations limiting prepayment penalties. Their enforcement priorities have centered on discriminatory rate-setting, dealer compensation arrangements, and protections for military personnel under the Military Lending Act.

The Servicemembers Civil Relief Act offers certain safeguards for active-duty military members, though it doesn't specifically prohibit prepayment penalties. Service members securing lower rates through SCRA provisions should confirm whether their initial loan's penalty language remains applicable.

Federal credit unions frequently eliminate prepayment penalties voluntarily as part of member-oriented service philosophies, despite facing no legal requirement to do so. This competitive positioning has influenced some commercial lenders to adopt similar approaches.

Author: Brandon Ellsworth;

Source: ruralxchange.net

How to Get a Car Loan Without Prepayment Penalty

Securing a no prepayment penalty car loan starts with asking pointed questions before signature. Throughout the application conversation, declare explicitly: "I need written confirmation that this financing contains zero prepayment penalties or early termination charges under any circumstances."

Credit unions historically provide more borrower-advantageous conditions than commercial banks or manufacturer-affiliated finance companies. Many credit unions maintain institutional policies against prepayment penalties, viewing them as inconsistent with their organizational purpose of supporting member financial wellness. Navy Federal, Pentagon Federal, and Alliant Credit Union specifically promote penalty-free conditions in their auto loan marketing.

Digital-first lenders including LightStream (operating under Truist) and PenFed highlight their absence of prepayment penalties as a marketplace differentiator. Their reduced operational overhead enables adequate profitability from interest income alone without requiring penalty provisions.

When discussing terms with a dealer's finance department, address this matter directly: "I'll only accept financing without prepayment penalties. Can you identify options satisfying this requirement?" Finance managers maintain connections with numerous lending institutions and can frequently submit your application to those providing penalty-free products.

Examine the financing agreement before signing, even when you're at the dealership experiencing pressure to finalize the transaction. Discovering a prepayment penalty provision that wasn't previously mentioned justifies refusing signature until the lender presents alternative conditions. Dealers prioritize completing sales and will often locate different financing rather than forfeit your business.

Obtaining preliminary approval from your banking institution or credit union before visiting dealerships provides leverage. Preliminary approval establishes a comparison benchmark against dealer-arranged financing. When your pre-approved financing lacks penalties but the dealer's proposal includes them, you possess clear bargaining power or can simply proceed with your preliminary approval.

Borrowers maintaining excellent credit profiles (scores exceeding 740) command the strongest negotiating positions. Lenders pursue low-risk borrowers aggressively, simplifying efforts to demand penalty-free conditions. Those with challenged credit encounter more constrained options but should still inquire and evaluate multiple lenders.

When Paying Off Your Car Loan Early Still Makes Sense

Even when facing a prepayment penalty, eliminating your debt ahead of schedule can generate savings if the penalty costs less than your remaining interest obligations. Perform calculations before committing to a decision.

Determine your remaining interest by obtaining a loan amortization breakdown from your lender or employing web-based calculation tools. Suppose you're 24 months into a 72-month loan at 7% interest on an initial $25,000 balance. You might owe $17,000 in outstanding principal and face approximately $3,200 in interest charges across the remaining 48 months.

Author: Brandon Ellsworth;

Source: ruralxchange.net

When your prepayment penalty equals 1% of remaining balance ($170), immediate settlement saves roughly $3,030 ($3,200 less $170). Higher interest rates and longer remaining loan periods increase the likelihood that early settlement provides net financial benefit despite penalty costs.

Evaluate opportunity costs carefully. Maintaining $17,000 in savings earning 4.5% in a high-yield account while continuing regular loan payments might prove wiser than settling a 7% loan with penalties attached. However, the guaranteed 7% "gain" from debt elimination frequently surpasses uncertain investment returns.

Early settlement makes particular sense during vehicle sales. Trading in or conducting private sales requires loan settlement regardless of timing. The penalty becomes unavoidable, though at least you're not maintaining debt obligations going forward.

Moving your debt to lower-rate financing might activate your existing loan's prepayment penalty, but substantially reduced rates quickly offset that expense. Refinancing from 9% to 4% on $20,000 remaining with 36 months outstanding saves roughly $1,500 in interest. Even a $400 penalty leaves you $1,100 better off financially.

Psychological considerations carry weight too. Certain borrowers value the emotional relief from eliminating debt obligations, even when mathematical analysis suggests deploying surplus funds elsewhere might generate superior returns. When debt generates anxiety and you can afford the penalty, the mental wellness advantage might validate the expense.

Alternatives to Full Early Payoff

When a prepayment penalty makes complete early settlement financially unattractive, you can still minimize interest expenses through strategic supplementary payments.

Most auto financing permits additional principal contributions without penalties, even though complete settlement triggers charges. Verify with your lender: "Can I contribute extra amounts toward principal without incurring charges?" Nearly all confirm this flexibility. Specify that supplementary payments apply to principal rather than advancing interest obligations, ensuring maximum advantage.

Contributing an additional $100 monthly on a $20,000 loan at 6% across five years saves roughly $1,300 in interest and shortens the term by approximately ten months. You're not technically settling early—you're accelerating contributions within the original framework.

Bi-weekly contribution approaches involve submitting half your monthly obligation every two weeks. With 52 weeks annually, you make 26 half-contributions (matching 13 full monthly obligations rather than 12). This supplementary annual contribution reduces principal faster without activating early settlement penalties.

Some borrowers contribute one substantial supplementary payment yearly—perhaps using tax refunds or year-end bonuses—to reduce principal without completely retiring the obligation. This method provides interest reduction while circumventing the penalty that full settlement would trigger.

Debt refinancing demands thorough evaluation. When your existing loan includes a prepayment penalty but you can refinance to lower rates with penalty-free new financing, calculate whether interest savings surpass penalty expenses. Factor in refinancing costs as well, typically ranging from zero to $500 depending on the institution.

Verify your loan's penalty timeframe. When you're 18 months into financing with a 24-month penalty window, delaying complete settlement six months to avoid penalties might prove smarter than paying penalties immediately. Calendar the penalty expiration date, then implement your early settlement approach.

Auto loan prepayment penalties are declining in frequency as borrower education improves and lender competition intensifies, but they remain present in the marketplace. Customers must scrutinize their contracts thoroughly and pose direct questions. The institutions most inclined to incorporate these charges are subprime finance operations serving credit-challenged customers. With decent credit standing, you should certainly be capable of securing competitive financing free of prepayment penalties

— Michael Chen

Frequently Asked Questions About Car Loan Prepayment Penalties

Financing your car loan without prepayment penalty provides freedom to eliminate debt ahead of schedule without monetary punishment, potentially conserving hundreds or thousands in interest expenses. While these penalties don't appear universally, they surface frequently enough that every borrower should confirm their financing conditions before executing agreements.

The most successful approach is prevention: shop deliberately for penalty-free financing, pose direct questions throughout the application conversation, and scrutinize your contract comprehensively before finalizing any agreement. Credit unions, digital lenders, and numerous banks now compete using borrower-advantageous terms, making penalty-free financing available to those maintaining reasonable credit.

When you already hold financing with a prepayment penalty, determine whether early settlement still generates financial advantage by comparing penalty costs against remaining interest obligations. Frequently, particularly with high-rate financing or substantial remaining terms, absorbing the penalty still produces net savings.

For those wanting to minimize interest expenses without activating penalties, supplementary principal contributions and bi-weekly payment approaches offer compromise solutions. These methods hasten debt elimination while operating within your financing's existing framework.

State regulations offer limited protection, while federal law remains largely uninvolved with auto loan prepayment penalties. This reality makes personal diligence your strongest protection. Whether shopping for new financing or assessing your existing loan, understanding prepayment penalties enables informed choices aligning with your financial objectives and potentially conserving substantial money across your vehicle loan's duration.

Related Stories

Read more

Read more

The content on this website is provided for informational and educational purposes only. It offers general guidance on topics related to car loans, auto refinancing, interest rates, credit scores, loan terms, and vehicle financing options. The information presented should not be considered financial, legal, or professional advice.

Auto loan terms, interest rates, approval requirements, and refinancing options may vary depending on the lender, credit profile, and individual circumstances.

While we aim to keep the information accurate and up to date, we make no guarantees regarding its completeness or reliability. Visitors should review official loan documents and consult with qualified financial professionals before making decisions related to auto loans or refinancing.