Buyer reviewing car loan options at a dealership next to a vehicle

How to Calculate Your Payment on a 25000 Car Loan

Ever walked into a dealership without knowing your numbers? That's where buyers lose leverage. When you're looking at a $25,000 vehicle—or really any car purchase—the difference between guessing and knowing can cost you thousands over the loan's life.

Here's what many shoppers don't realize: a $25,000 loan at 6% stretched over five years will run you about $483 each month. Push that same loan to six years and your monthly bill drops to $414, which sounds great until you realize you've just added nearly $600 in extra interest charges. Not so great anymore.

We're breaking down everything that goes into car loan math—what you'll actually pay on loans from $8,000 up to $25,000, how lenders decide your rate, and concrete ways to trim your monthly bill without settling for a worse vehicle.

How Car Loan Payments Are Calculated

Your monthly car payment splits into two chunks: principal and interest. The principal is straightforward—it's the actual cash you borrowed. Interest is what the bank charges for letting you use that money.

Here's the quirky part most people miss. Those first few payments? You're mostly paying interest. Very little chips away at what you actually owe. But as months pass and your balance drops, more of each payment tackles the principal. By your final year, you're knocking down the actual debt much faster.

Let's decode that: - M is what you pay monthly - P is how much you're borrowing - r is your monthly interest rate (grab the annual rate and slice it into 12 pieces) - n counts your total monthly payments

Don't worry—you won't need to solve this by hand. Every bank has calculators that do the heavy lifting. Still, understanding these pieces explains why bumping from 6% to 8% interest tacks on about $30 monthly for a $25,000 loan. Or why choosing 72 months instead of 60 cuts your payment but inflates your total cost.

One trap catches nearly everyone: that sticker price isn't what you're financing. Take that $25,000 car, put $3,000 down, and suddenly you're only borrowing $22,000. Same goes for trade-ins and rebates—they all reduce what you actually need to finance, which means lower payments.

Author: Olivia Stratford;

Source: ruralxchange.net

Factors That Affect Your Monthly Car Payment

Interest rate rules everything. Excellent credit might land you 4.5% on a new car right now in 2026. Fair credit? You're probably looking at 9% or worse. Let's put real numbers to that: borrowing $25,000 for 60 months at 4.5% means paying $467 monthly. At 9%, that jumps to $519. We're talking $52 more every single month—$3,120 over five years just because of your credit score.

Loan term sets how long you're making payments. Longer terms shrink individual payments but pile on total interest. Shorter terms build equity faster and save money overall, assuming your budget can handle the bigger monthly hit.

Down payment does the simplest thing: it cuts what you need to borrow. Drop $5,000 on that $25,000 car and you're only financing $20,000. At 6% over 60 months, your payment falls from $483 to $386. That's $97 back in your pocket every month.

Credit score decides what rate lenders quote you. Above 720? You're golden—expect their best offers. Between 620 and 680? You'll pay more. Below 600 typically means subprime territory with rates hitting double digits, if you even get approved.

Sales tax, registration, and dealer fees sneak into your loan when you don't pay them upfront. A state charging 7% sales tax adds $1,750 to a $25,000 deal. Finance that extra chunk and you've just bumped your monthly payment by roughly $34 for the next five years.

Sample Monthly Payments by Loan Amount

Here's what different loan amounts actually cost monthly, assuming you qualified for a 6% rate:

| Loan Amount | 48 Months @ 6% | 60 Months @ 6% | 72 Months @ 6% |

| $8,000 | $188 | $155 | $133 |

| $10,000 | $235 | $193 | $166 |

| $16,000 | $376 | $309 | $266 |

| $17,000 | $399 | $329 | $283 |

| $25,000 | $587 | $483 | $414 |

These numbers assume decent credit getting you that 6% rate. Your actual payment depends entirely on what rate your lender approves.

Notice how payments on a 10000 car loan drop from $235 to $193 when you extend from 48 to 60 months? Sounds good, except you're giving up about $180 more in interest. For an 8000 car loan monthly payment, the difference between 48 and 72 months is $55—meaningful if you're watching every dollar.

A payment on 16000 car loan running 60 months ($309) fits many budgets comfortably. Payments on 17000 car loan only add $20 monthly. Small loan differences don't dramatically shift affordability. Rate and term length? Those absolutely do.

How Interest Rates Change Your Payment

Rate changes create massive payment swings. Look at what happens with that $25,000 loan:

| Interest Rate | 48-Month Payment | 60-Month Payment | Total Interest Paid (60 mo) |

| 4% | $564 | $460 | $2,600 |

| 6% | $587 | $483 | $3,980 |

| 8% | $610 | $507 | $5,420 |

| 10% | $634 | $531 | $6,860 |

Going from 4% to 10% means paying $71 more monthly on a 60-month loan, plus you're hemorrhaging an extra $4,260 in interest. That's used car money right there.

Even a two-point gap matters. Get 6% instead of 8%—maybe by improving your credit or shopping harder—and you're saving $24 monthly, $1,440 total on that $25,000 loan over five years.

Dealers love advertising 0.9% or 1.9% rates. Catch: those usually require 750+ credit scores and you might have to give up cash rebates. Always run both scenarios. Sometimes grabbing a $2,000 manufacturer rebate with 6% financing beats taking 1.9% with no rebate.

Author: Olivia Stratford;

Source: ruralxchange.net

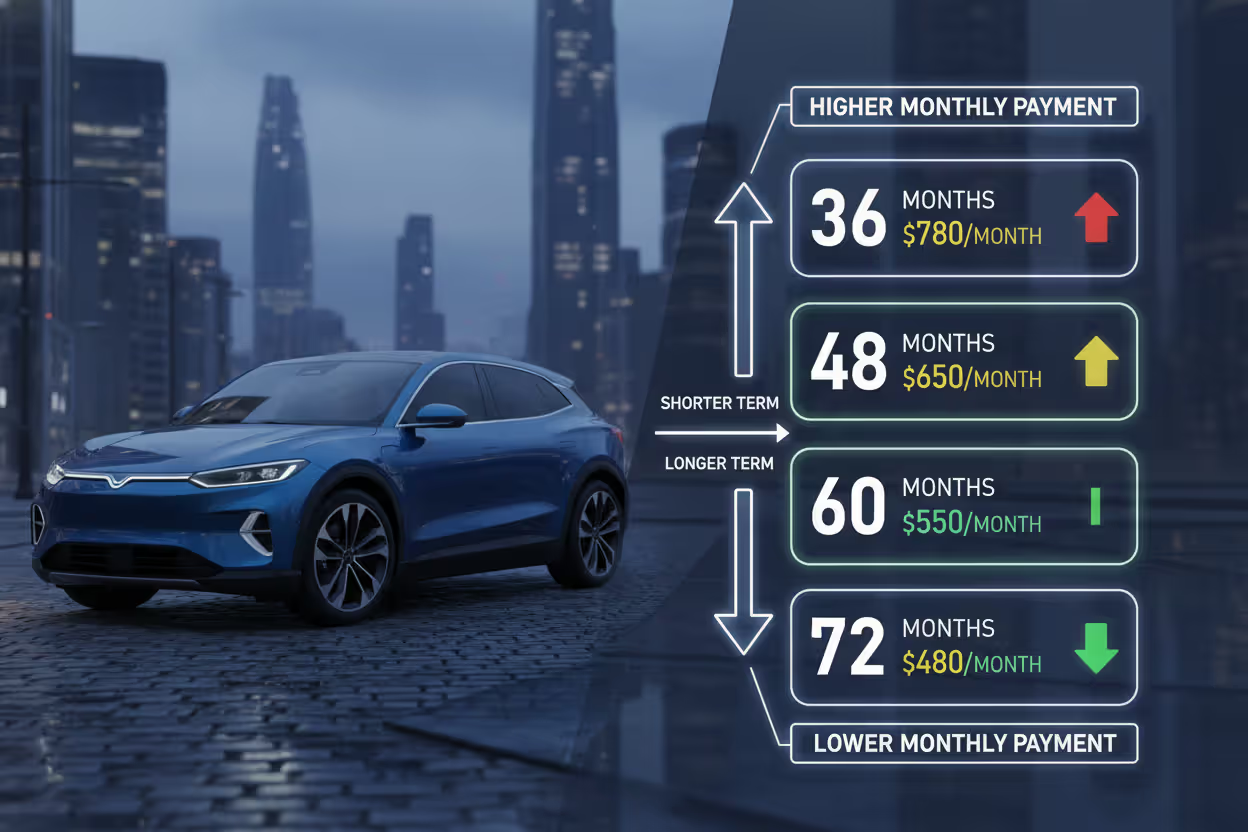

Choosing the Right Loan Term for Your Budget

36-month loans cut total interest to the bone and get you to ownership fast. Three years from now, you own the car outright. If it's still worth $15,000, that's pure equity in your hands. Downside? Big monthly payments. That $25,000 loan at 6% means forking over $761 monthly—doable if you're earning well, brutal otherwise.

48-month loans balance affordability with reasonable interest costs. You'll pay somewhat more interest than a three-year loan but way less than longer terms. This sweet spot works for buyers who want to limit interest without crushing their monthly budget.

60-month loans dominate the market because they deliver manageable payments without trapping you underwater (owing more than the car's worth) for too long. A payment on a 10000 car loan over 60 months at 6% hits $193—achievable for most budgets. Well-maintained cars usually hold enough value at five years to avoid that underwater scenario.

72-month loans and beyond slash monthly payments substantially but create real hazards. Cars depreciate faster than you build equity in those early years, which means trouble if you need to sell or trade. Plus you're surrendering considerably more to interest. That $25,000 loan costs $3,980 in interest over 60 months but $4,920 over 72 months—an extra $940 you're paying just for convenience.

Rule of thumb: never finance longer than you plan to keep the car. Trade every four years? Then 72-month financing guarantees you'll still owe money when you're ready to move on.

Author: Olivia Stratford;

Source: ruralxchange.net

How to Lower Your Monthly Car Payment

Increase your upfront cash. Every $1,000 you put down cuts roughly $20 from your monthly payment on a 60-month loan. Save $4,000 instead of $2,000 and you've dropped your payment by $40 monthly. Trading in your current car? Roll that equity straight into your down payment.

Fix your credit before you shop. Boosting your score from 650 to 720 can slice interest rates by two or three full percentage points. Pay down credit cards below 30% of their limits. Dispute errors on your credit report—they're more common than you think. Stop applying for new credit cards in the months before you need a car loan. Six months of focused credit work can save thousands in interest.

Author: Olivia Stratford;

Source: ruralxchange.net

Shop multiple lenders. Never take the dealer's first financing offer without checking alternatives. Get pre-approved by your bank or credit union before stepping onto a dealer lot—credit unions often beat dealer rates by a full point or more. Online lenders and regional banks deserve a look too. Walking in with pre-approval gives you serious negotiating power.

Consider certified pre-owned instead of new. Cars two years old cost 20-30% less than identical new models while offering most of the useful life, often with warranty coverage still active. That $25,000 new car? A comparable certified pre-owned around $18,000 drops your payment from $483 to $348 monthly.

Negotiate price separately from payment. Dealers love when you focus only on monthly payment because they can juggle loan length, sneak in extras, or inflate the price while keeping you at your magic number. Lock down the vehicle's final price first. Then handle financing as its own separate deal.

Skip unnecessary add-ons. Extended warranties, paint protection, gap insurance—these get rolled into your loan and jack up monthly costs. A $2,000 warranty added to a $25,000 loan at 6% over 60 months increases your payment by $39 monthly. Only buy protections you genuinely need, and check if third-party providers offer better deals.

Financial experts recommend keeping your total car payment under 15% of your monthly take-home pay to maintain a healthy budget. When you include insurance, fuel, and maintenance, your total transportation costs should stay below 20% of income

— Jennifer Martinez

Frequently Asked Questions About Car Loan Payments

Car financing stops being intimidating once you understand how it actually works. Whether you're figuring out the payment on a 25000 car loan or exploring smaller financing amounts, the fundamentals stay the same: lower rates, shorter terms, and bigger down payments all reduce both monthly costs and lifetime expense.

The trick is finding what fits your specific situation. A $400 monthly payment might feel comfortable for one household but squeeze another's finances dangerously tight. Use these tables and examples as starting points, then adjust for your actual interest rate, down payment, and chosen term.

Before signing anything, confirm that total car expenses—payment, insurance, gas, maintenance—don't exceed 15-20% of your take-home pay. That buffer protects you if circumstances change and prevents sacrificing other financial goals just to keep a car.

Spend time comparing both vehicles and financing sources. An hour evaluating lender rates could save you $1,000 or more over your loan's life. Remember: the best car loan is one you can afford comfortably while still building emergency savings and pursuing your other financial priorities.

Related Stories

Read more

Read more

The content on this website is provided for informational and educational purposes only. It offers general guidance on topics related to car loans, auto refinancing, interest rates, credit scores, loan terms, and vehicle financing options. The information presented should not be considered financial, legal, or professional advice.

Auto loan terms, interest rates, approval requirements, and refinancing options may vary depending on the lender, credit profile, and individual circumstances.

While we aim to keep the information accurate and up to date, we make no guarantees regarding its completeness or reliability. Visitors should review official loan documents and consult with qualified financial professionals before making decisions related to auto loans or refinancing.