Car loan documents, car keys, and amortization schedule on a desk

Car Loan Calculator with Amortization Schedule

When you finance a vehicle, understanding exactly where your money goes each month can save you thousands of dollars over the life of the loan. Most borrowers focus only on the monthly payment amount, but the breakdown of principal versus interest tells a far more important story about the true cost of your auto financing.

An amortization schedule transforms your car loan from an abstract debt into a transparent roadmap. You'll see precisely how much of each payment reduces your actual loan balance and how much simply covers the lender's interest charges. This visibility empowers you to make smarter decisions about extra payments, refinancing opportunities, and whether that extended loan term actually makes financial sense.

What Is a Car Loan Amortization Schedule?

A car loan amortization schedule is a detailed table that breaks down every single payment you'll make over your loan's lifetime. Each row represents one month, showing four critical numbers: your total payment amount, how much goes toward principal, how much covers interest, and your remaining balance after that payment posts.

The term "amortization" refers to the process of gradually paying off debt through regular installments. Unlike interest-only loans where your balance never decreases, an amortized car loan ensures that every payment chips away at what you actually owe, even if progress feels slow at first.

For borrowers, this schedule matters because it reveals the hidden cost of financing. You might see a $450 monthly payment and think that sounds manageable, but the amortization table for car loan shows that $320 of your first payment goes straight to interest while only $130 reduces your debt. That reality check often motivates people to reconsider their down payment amount or loan term.

Banks and credit unions use amortization schedules to calculate your exact payment amount. The math ensures that if you make every scheduled payment on time, your final payment will bring your balance to exactly zero. No surprises, no balloon payments, just a predictable path to ownership.

Author: Samantha Whitaker;

Source: ruralxchange.net

How Car Loan Amortization Works

Car loans use simple interest calculated on your remaining balance. Each month, the lender multiplies your current balance by your monthly interest rate (annual rate divided by twelve), determines the interest charge, then applies the remainder of your payment to principal.

This front-loaded interest structure means your early payments accomplish remarkably little debt reduction. On a $30,000 loan at 7% APR over 60 months, your first payment might be $594, but only $419 reduces principal while $175 goes to interest. By month 30, that ratio shifts to $485 principal and $109 interest. Your final payment will be almost entirely principal.

The reason? You're always paying interest on whatever you still owe. When you owe $30,000, interest charges are substantial. When you owe $5,000, they're minimal. Your payment amount stays constant, but the composition changes dramatically.

Principal vs. Interest Over Time

Think of your auto loan amortization schedule calculator results as a seesaw. Early in the loan, interest sits heavy on one side while principal barely registers. Month by month, the balance shifts until principal dominates and interest becomes negligible.

This shift accelerates as you progress. The reduction in your balance from month 1 to month 2 might be $130, but from month 35 to month 36 it could be $280, even though your payment amount never changed. Each dollar of principal you eliminate means less interest accrues the following month, creating a snowball effect.

For a concrete example: on that $30,000 loan, you might pay $5,250 in interest over the first 30 months but only $1,380 over the final 30 months, despite making identical payments throughout.

Why Early Payments Go Mostly to Interest

Lenders don't structure loans this way to trick you. The math simply reflects how interest works. You borrowed a large sum, and interest is the cost of using someone else's money. When you've used $30,000 of their money for a month, the charge is higher than when you've only used $10,000.

Some borrowers mistakenly believe lenders "front-load" interest as a profit-maximizing scheme. In reality, if you paid the loan off after 12 months, you'd only pay 12 months of interest. The schedule simply shows what happens if you make minimum payments for the full term.

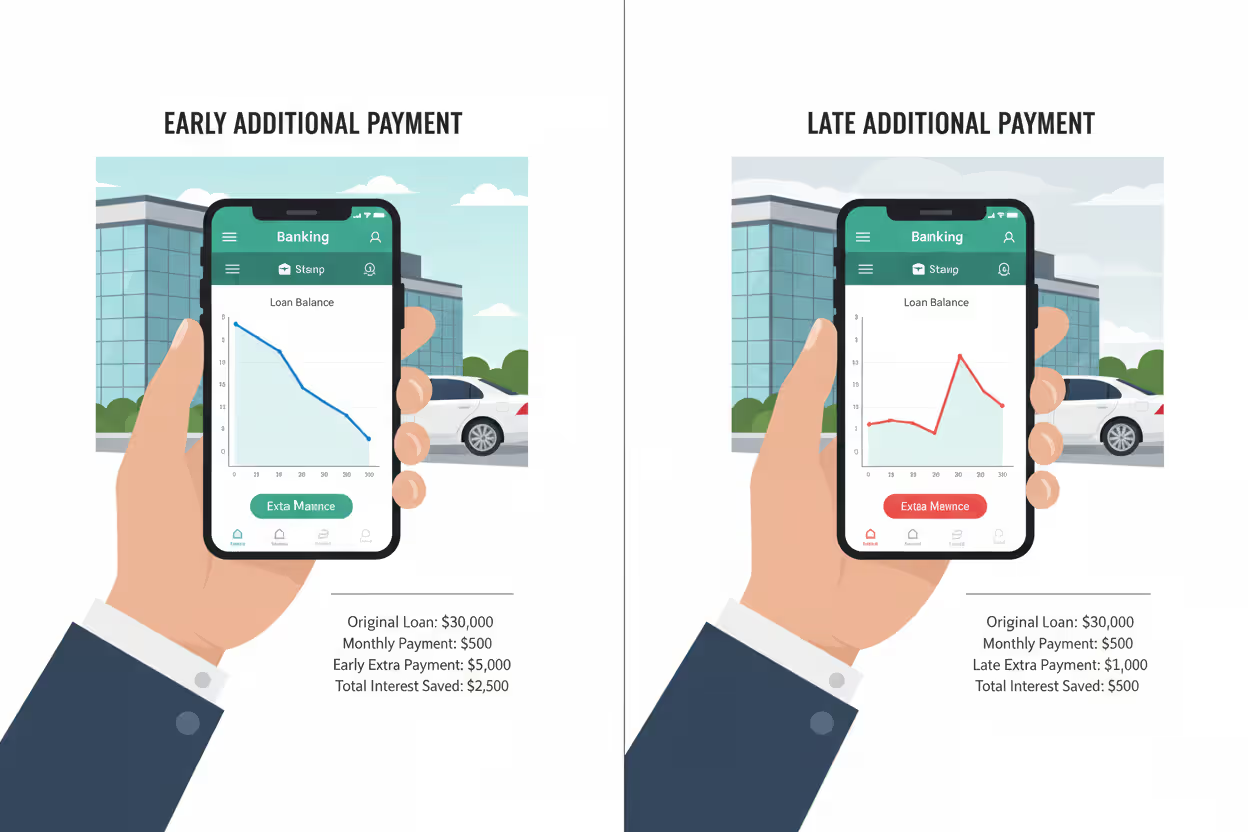

This structure has one major implication: extra payments made early in your loan have outsized impact. A $1,000 extra payment in month 6 eliminates principal that would have accrued interest for the next 54 months. That same $1,000 in month 54 only saves six months of interest charges.

Author: Samantha Whitaker;

Source: ruralxchange.net

How to Use a Car Loan Amortization Calculator

Most car loan amortization calculator monthly tools require just four inputs: loan amount, interest rate, loan term, and start date. Getting these numbers right makes the difference between useful projections and garbage data.

Loan amount: Enter the amount you're actually financing, not the vehicle's price. If you're putting $5,000 down on a $28,000 car, enter $23,000. Some calculators let you add taxes, fees, and trade-in equity, which is helpful since most buyers finance the out-the-door cost minus their down payment.

Interest rate: Use your actual APR as a percentage. If your approval letter says 6.49%, enter 6.49, not 0.0649. Double-check whether your lender quoted APR or a simple interest rate; for car loans, these are typically the same, but dealer financing sometimes uses different terminology.

Loan term: Enter the number of months, usually 36, 48, 60, or 72. Longer terms lower your payment but dramatically increase total interest. A calculator lets you compare scenarios side-by-side.

Start date: This seems minor but affects your first payment date and helps you align the schedule with your actual loan documents. Most calculators default to the current month.

After entering these details, the calculator displays your monthly payment amount and generates a complete payment schedule. Quality calculators also show total interest paid, total amount paid, and payoff date. Some let you model extra payments to see how much time and money you'd save.

Spend time comparing scenarios. Run the numbers with different down payments, terms, and interest rates. You might discover that a 48-month loan at 5.9% costs less overall than a 60-month loan at 5.5%, even though the rate is higher, because you're paying interest for fewer months.

Author: Samantha Whitaker;

Source: ruralxchange.net

Reading Your Car Payment Amortization Schedule

The amortization table contains six columns, each telling part of your loan's story. Understanding what you're looking at transforms raw numbers into actionable insights.

Payment number: Simply counts from 1 to your total number of payments. Month 1 is your first payment, usually due 30-45 days after you sign the paperwork.

Payment date: Shows when each payment is due. Missing these dates triggers late fees and potentially damages your credit, so this column helps you plan ahead.

Payment amount: Your regular monthly payment, which stays constant for the entire loan (unless you have a variable-rate loan, which is rare for auto financing). This amount covers both principal and interest.

Principal paid: The portion of your payment that reduces your actual debt. This number starts small and grows with each payment. It's the only part of your payment that builds equity.

Interest paid: The portion that compensates your lender. This starts large and shrinks over time. It's pure cost—you get nothing tangible in return except the privilege of borrowing money.

Remaining balance: What you still owe after each payment posts. This number should decrease every month. If you're considering selling the car or refinancing, this column shows your exact payoff amount at any point.

Look for the crossover point where principal paid exceeds interest paid. On a 60-month loan, this often happens around month 30-35. Before that point, you're paying more in interest than debt reduction each month. After it, you're finally making serious progress.

Here's a sample car payment amortization schedule for a $25,000 loan at 6% APR over 60 months (monthly payment: $483.32):

| Payment # | Payment Amount | Principal Paid | Interest Paid | Remaining Balance |

| 1 | $483.32 | $358.32 | $125.00 | $24,641.68 |

| 6 | $483.32 | $377.13 | $106.19 | $22,719.86 |

| 12 | $483.32 | $396.90 | $86.42 | $20,381.48 |

| 24 | $483.32 | $439.88 | $43.44 | $15,134.22 |

| 36 | $483.32 | $457.72 | $25.60 | $9,520.86 |

| 48 | $483.32 | $476.40 | $6.92 | $3,536.44 |

| 60 | $483.32 | $480.91 | $2.41 | $0.00 |

Notice how the principal paid increases from $358 to $481 while interest drops from $125 to just $2. The total interest paid over all 60 months would be $3,999.20, meaning this $25,000 loan actually costs $28,999.20.

Benefits of Reviewing Your Auto Loan Payoff Schedule

Most people glance at their loan paperwork once, then ignore it until payoff. That's a costly mistake. Your car loan payoff schedule calculator results deserve regular attention for several strategic reasons.

Financial planning accuracy: When you know exactly what you'll owe in month 24 or month 48, you can make informed decisions about trading in your vehicle. Many borrowers end up underwater—owing more than the car is worth—because they didn't check their amortization schedule before visiting the dealership.

Early payoff strategies: The schedule shows you precisely how much extra payment is needed to eliminate specific months from your loan. Want to pay off your loan six months early? Add up the principal portions of your final six payments, and that's your target amount. Some borrowers systematically pay one extra month of principal every quarter, shaving a full year off a 60-month loan.

Refinancing decisions: When interest rates drop or your credit improves, your amortization schedule helps you calculate whether refinancing makes sense. If you've already paid through the high-interest early months, refinancing might not save as much as you expect. Run the numbers for your current remaining balance and compare.

Total interest awareness: Seeing "$8,400 in interest charges" as an abstract concept doesn't hit as hard as watching it accumulate month by month in your amortization table. This awareness often motivates borrowers to increase their payment amount or make periodic extra payments, especially in the first two years when interest charges are highest.

Negotiating leverage: When shopping for a car loan, bringing amortization schedules from competing lenders to the negotiating table demonstrates financial literacy. Dealers and lenders treat informed borrowers differently than those who focus only on monthly payment amounts.

Some borrowers print their amortization schedule and mark off each payment as they make it. This simple habit creates psychological momentum and keeps your payoff date front-of-mind rather than abstract and distant.

Author: Samantha Whitaker;

Source: ruralxchange.net

Common Mistakes When Using Car Loan Calculators

Even straightforward calculators produce misleading results when fed incorrect information. Watch for these frequent errors that skew your projections.

Wrong interest rate format: Entering 0.065 instead of 6.5 will calculate interest at 0.065%, giving you absurdly low payment estimates. Conversely, entering 650 instead of 6.5 produces impossibly high numbers. Most calculators expect the rate as a percentage (6.5), but some want decimal format (0.065). Check the label or try a known example to verify.

Ignoring fees and taxes: Your loan amount should include everything you're financing—sales tax, registration, dealer fees, extended warranties you agreed to purchase. If you're financing $28,000 but only enter the $25,000 vehicle price, your entire schedule will be off by $3,000.

Misunderstanding APR vs. interest rate: For car loans, these are usually identical, but some promotional financing uses different terms. APR includes certain fees and represents the true cost of borrowing. If your paperwork shows both numbers, use APR for the most accurate amortization schedule.

Not accounting for down payment: If you're buying a $30,000 car with $6,000 down, you're financing $24,000 (plus fees and taxes). Entering $30,000 in the calculator will show payments for a loan you're not actually taking.

Forgetting trade-in equity: Trading in a paid-off vehicle worth $8,000 is functionally identical to making an $8,000 down payment. Subtract this from your loan amount. If you still owe money on your trade-in, the situation gets more complex—dealers typically pay off your old loan and roll any shortfall into your new loan.

Assuming biweekly payments work like monthly: Some calculators offer biweekly payment options, which result in 26 half-payments per year (equivalent to 13 full monthly payments). This isn't the same as simply dividing your monthly payment by two. The extra payment each year significantly reduces your loan term and interest charges, but you need to model it correctly.

Overlooking prepayment penalties: While rare on modern car loans, some lenders charge fees if you pay off your loan early. If your loan has this clause, the amortization schedule's interest savings from extra payments might be partially offset by penalties. Check your loan agreement.

Most car buyers spend hours researching the vehicle itself but less than 20 minutes understanding their loan structure. Your amortization schedule is a financial X-ray of your loan—it shows you exactly what you're paying for and when. Borrowers who study their schedule before signing typically negotiate better terms and pay off their loans 15-20% faster than those who focus only on the monthly payment amount

— Jennifer Martinez

FAQ

Your car loan amortization schedule transforms abstract monthly payments into a concrete roadmap of debt elimination. By understanding how each payment splits between principal and interest, you gain the insight needed to make strategic decisions about extra payments, refinancing, and loan terms.

The front-loaded interest structure means your early payments accomplish less debt reduction than you might expect, but this same structure makes extra payments in the first half of your loan remarkably powerful. Even modest additional payments can shave months off your loan and save hundreds or thousands in interest charges.

Before signing any car loan, run the numbers through a calculator and study the resulting amortization table. Compare different scenarios with various down payments, interest rates, and loan terms. The few minutes you invest in understanding these numbers will pay dividends throughout your loan's life and help you avoid the costly mistakes that trap many borrowers in extended, high-interest auto debt.

Related Stories

Read more

Read more

The content on this website is provided for informational and educational purposes only. It offers general guidance on topics related to car loans, auto refinancing, interest rates, credit scores, loan terms, and vehicle financing options. The information presented should not be considered financial, legal, or professional advice.

Auto loan terms, interest rates, approval requirements, and refinancing options may vary depending on the lender, credit profile, and individual circumstances.

While we aim to keep the information accurate and up to date, we make no guarantees regarding its completeness or reliability. Visitors should review official loan documents and consult with qualified financial professionals before making decisions related to auto loans or refinancing.