Driver reviewing insurance documents beside a damaged car after an accident

What to Do If Your Car Totaled Still Owe on Loan

Getting into an accident is stressful enough. Learning that your insurance check won't cover what you owe on your car loan adds financial pain to an already difficult situation. Thousands of American drivers face this scenario every year, discovering they're responsible for a loan on a vehicle they can no longer drive.

When your insurance company declares your vehicle a total loss, they pay you the actual cash value—not what you financed. That gap between the payout and your remaining loan balance becomes your problem to solve. Understanding your obligations and available options can help you navigate this challenging financial situation without damaging your credit or draining your savings.

What Happens When Your Car Is Totaled and You Still Owe Money

Insurance companies declare a vehicle totaled when repair costs exceed a certain percentage of its actual cash value (ACV)—typically 70-80%, depending on your state. The insurer pays you the ACV, which reflects what your vehicle was worth immediately before the accident, accounting for depreciation, mileage, and condition.

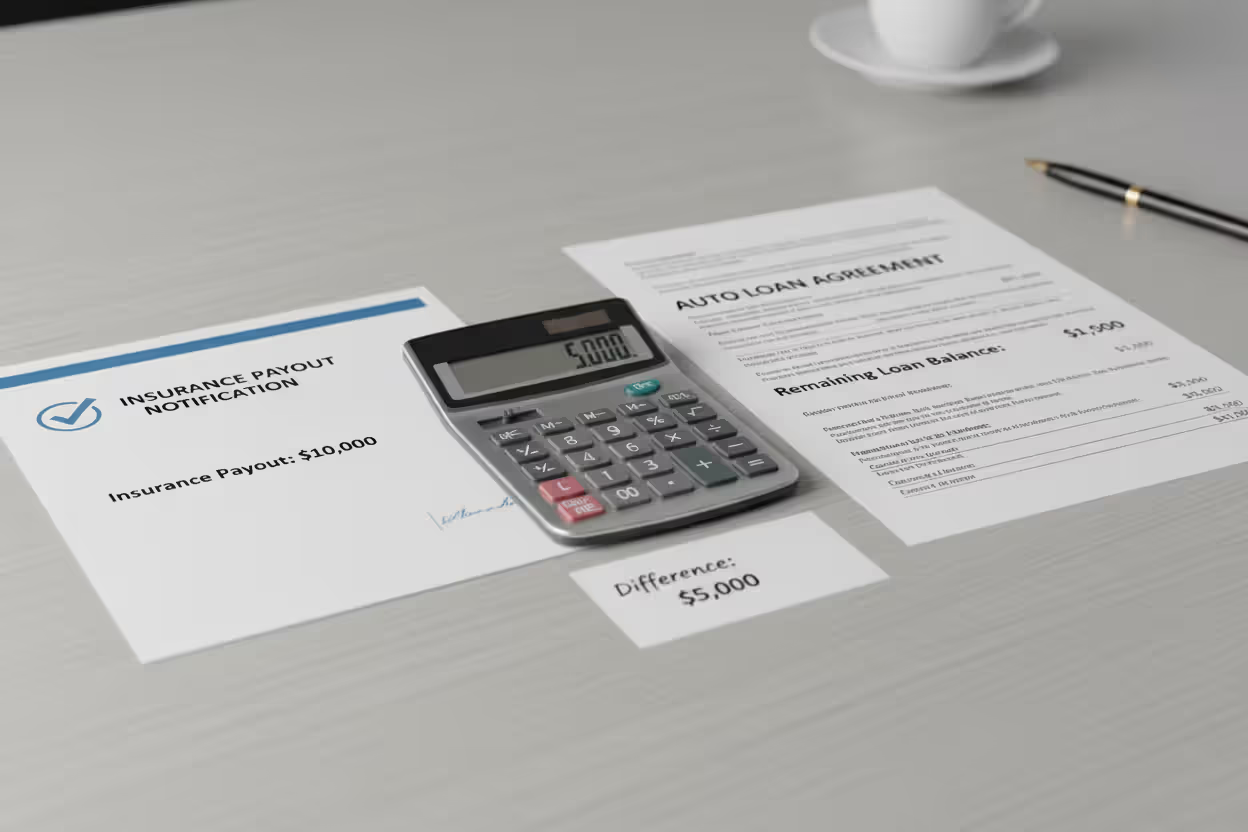

Here's where the problem emerges: your lender doesn't care about actual cash value. They care about the remaining principal balance on your auto loan. If you owe $22,000 but your totaled car with loan balance receives an insurance payout of only $18,000, you're responsible for the $4,000 difference.

The insurance payment goes directly to your lender if they hold the title as a lienholder. You don't get to pocket that money and decide whether to pay the loan. The lender receives their portion first, and if there's any surplus after the loan is satisfied, you receive the remainder. When there's a shortfall, your lender will send you a bill for the deficiency.

Author: Olivia Stratford;

Source: ruralxchange.net

Financial experts refer to this predicament as having negative equity in your vehicle—you owe more than the asset is worth. The vehicle that secured your loan no longer exists, but the debt remains fully enforceable. Your loan agreement doesn't include an escape clause for total loss accidents.

Why Insurance Payouts Are Often Less Than Your Loan Balance

Several factors create the gap between what you owe and what insurance pays. Understanding these helps explain why so many drivers end up with a car totaled with loan balance issues.

Depreciation happens faster than loan paydown. New vehicles lose 20-30% of their value the moment you drive off the lot. They continue depreciating 15-25% each subsequent year. Meanwhile, your loan balance decreases slowly, especially in the early years when most of your payment goes toward interest rather than principal. A car you bought for $30,000 might be worth $21,000 after one year, but you might still owe $26,000 on a 72-month loan.

High-interest loans amplify the problem. Borrowers with subprime credit often face interest rates of 10-20% or higher. More of each monthly payment services interest rather than reducing the principal balance. You make payments for months yet barely dent what you owe.

Minimal down payments leave no equity cushion. Putting down less than 20% means you start with little to no equity from day one. Some buyers put down nothing at all, financing taxes, fees, and dealer add-ons. You're immediately behind the depreciation curve.

Previous vehicle debt rolled into new financing adds thousands to your new loan. When your trade-in has an outstanding balance exceeding its market value by $5,000, dealers often finance that shortfall into your new purchase. You're now paying interest on money that bought a vehicle you no longer own.

Extended loan terms of 72, 84, or even 96 months spread payments so thin that principal reduction crawls along. These loans keep you in a negative equity position for years. By the time you've built meaningful equity, the vehicle may need replacement anyway.

Author: Olivia Stratford;

Source: ruralxchange.net

Your Financial Responsibilities After a Total Loss

Do You Still Have to Pay the Remaining Loan Balance?

Yes, absolutely. The loan agreement you signed creates a legal obligation to repay the full amount borrowed, regardless of what happens to the vehicle. Total loss doesn't cancel debt.

Your lender will continue expecting payment on the remaining balance after applying the insurance payout. If you owe $5,000 after the insurance check, that becomes an unsecured debt—there's no collateral backing it anymore, but you're still legally required to pay.

Some borrowers mistakenly believe insurance "should" cover the full loan amount. Insurance companies only owe you the vehicle's actual value, not what you financed. That's the fundamental principle of property insurance: restoration to pre-loss condition, not profit or loan satisfaction.

The remaining balance typically becomes due immediately or converts to a personal loan with continued monthly payments. Your lender's policies determine the specific terms, but they won't simply forgive the difference.

What Happens If You Stop Making Payments

Defaulting on the remaining balance after a total loss carries serious consequences. Since the loan is now unsecured, the lender can't repossess anything—the car is gone—but they have other collection tools.

Expect significant damage to your credit profile. Missed payments appear on your credit report, and eventually the account goes into default. Your score can drop 100+ points, making future borrowing expensive or impossible. This affects everything from apartment rentals to job applications.

The lender may sue you for the deficiency. They can obtain a judgment, then garnish your wages (up to 25% of disposable earnings in most states), levy your bank accounts, or place liens on other property you own. Court costs and attorney fees get added to what you owe.

Debt collectors get involved. The lender may sell your debt to a collection agency that will aggressively pursue payment. Expect frequent calls, letters, and potential legal action. When creditors agree to accept less than you owe, that notation stays visible to future lenders for seven years.

Some borrowers consider bankruptcy, but this should be a last resort after exploring all other options. Bankruptcy has long-lasting consequences that extend far beyond a single car loan deficiency.

Gap Insurance and How It Protects You

Gap insurance—Guaranteed Asset Protection—covers the difference between your vehicle's actual cash value and your outstanding loan balance when you experience a total loss. It's specifically designed to solve the problem of owing on a car after total loss.

When your primary insurance pays $19,000 but you owe $24,000, gap insurance covers that $5,000 difference. The policy settles your entire debt with the lender, leaving you with zero financial obligation. The policy pays directly to the lienholder after your primary insurance settles.

Gap coverage typically costs $400-700 when purchased through a dealership as a one-time fee added to your loan, or $20-40 annually when added to your auto insurance policy. Buying through your insurer is almost always cheaper and can be canceled when you've built enough equity.

Author: Olivia Stratford;

Source: ruralxchange.net

Who should consider gap insurance?

- Anyone who put down less than 20%

- Buyers with loan terms longer than 60 months

- Drivers who rolled negative equity into their current loan

- Lessees (gap protection is often included in lease agreements)

- Owners of vehicles that depreciate rapidly

Gap insurance doesn't cover everything. It won't pay for: - Overdue loan payments before the total loss - Late fees or penalties - Extended warranties or other loan add-ons - Costs exceeding the policy's maximum coverage (usually 25% of ACV) - Lease penalties for excess wear or mileage

Filing a gap claim requires submitting your primary insurance settlement letter, loan payoff statement, and gap insurance claim form. The process typically takes 2-4 weeks after your primary claim settles. Your lender may require you to continue making payments until the gap insurer pays, though you'll be reimbursed.

Options When You Owe More Than the Insurance Payout

| Situation | Insurance Settlement | Outstanding Loan | Gap Policy Payout | Your Responsibility |

| Gap coverage in place | $18,000 | $23,000 | $5,000 | $0 |

| No gap coverage | $18,000 | $23,000 | $0 | $5,000 |

| Gap coverage with policy limits | $18,000 | $23,000 | $4,500 | $500 |

| No gap coverage, successfully negotiated higher ACV | $19,500 | $23,000 | $0 | $3,500 |

Negotiate With Your Insurance Company

Insurance companies use valuation tools and comparable vehicle sales to determine actual cash value, but these aren't infallible. You can challenge their assessment if you believe it's too low.

Research your vehicle's pre-accident condition and current market pricing. Collect recent maintenance records showing you kept the car in excellent condition. Find comparable vehicles for sale in your area—same year, make, model, mileage, and condition—listed at higher prices. Document any upgrades or modifications that add value.

Submit this evidence to your adjuster with a formal request to reconsider the valuation. Be professional and factual. Many insurers will increase their offer by $500-2,000 when presented with solid comparable sales data. This won't eliminate a large gap, but it reduces what you owe out of pocket.

Consider hiring an independent appraiser if the stakes are high enough. Their professional assessment carries weight with insurance companies. The appraisal might cost $200-400, worthwhile if you're fighting over several thousand dollars.

Pay the Difference Out of Pocket

The cleanest solution is paying the deficiency immediately if you have savings available. This closes the loan, protects your credit, and eliminates ongoing interest charges.

Before writing a check, confirm the exact payoff amount with your lender. Get it in writing. The figure they quote should account for the insurance payment they've already received. Ask whether they'll accept a slightly reduced settlement for immediate payment—some lenders will discount the balance by 10-20% to close the account quickly.

Paying the full amount hurts, especially after losing your vehicle, but it prevents months or years of continued payments on something you can't use. You're free to move forward without this debt hanging over you.

Refinance the Remaining Balance

Some lenders will convert the deficiency into a personal loan with structured monthly payments. This transforms the immediate crisis into a manageable payment plan, though you'll pay interest on money that once bought transportation you no longer have.

Personal loan rates for unsecured debt typically run 8-15% for borrowers with good credit, higher for those with challenged credit. Compare this to continuing the original auto loan terms, which might have a lower rate since it was secured by the vehicle.

Shop around. Credit unions often offer better rates on personal loans than banks or the original auto lender. A $4,000 deficiency on a 36-month personal loan at 10% costs about $129 monthly. That's more affordable than coming up with $4,000 immediately, though you'll pay roughly $640 in interest over the life of the loan.

Author: Olivia Stratford;

Source: ruralxchange.net

Settle With Your Lender

If you genuinely cannot pay the deficiency, contact your lender before you miss payments. Some will negotiate a settlement for less than the full balance, particularly if they believe you might otherwise default or file bankruptcy.

Most financial institutions prefer receiving partial payment over writing off the entire debt. They might accept 50-70% of the deficiency as payment in full. A $6,000 balance might settle for $3,500-4,000. Get any settlement agreement in writing before sending money, confirming they'll report the loan as "paid in full" or at minimum "settled" rather than "charged off."

Understand that settled accounts hurt your credit, though not as severely as defaults or charge-offs. This negative mark remains visible on credit reports for a full seven-year period. You may also owe income tax on the forgiven amount—the IRS considers forgiven debt as taxable income.

How to Avoid Owing Money on a Totaled Car in the Future

Author: Olivia Stratford;

Source: ruralxchange.net

Prevention beats cure when it comes to car loan after total loss situations. Several strategies protect you from ending up in a negative equity position.

Make a substantial down payment. Putting down 20% or more gives you an equity cushion from day one. Depreciation eats into your down payment rather than creating negative equity. You're less likely to owe more than the vehicle's worth at any point during the loan.

Purchase gap insurance when you buy or lease. This is non-negotiable if you're putting down less than 20%, financing for longer than 60 months, or rolling negative equity into your new loan. Add it to your auto insurance policy rather than buying through the dealership—you'll save hundreds and can cancel it once you've built equity.

Choose shorter loan terms. A 48-month loan builds equity much faster than a 72-month loan. Yes, the monthly payment is higher, but you're not in a vulnerable financial position for years. If you can't afford the payment on a 48-month loan, you're probably buying more car than you can comfortably afford.

Avoid rolling negative equity. If you have an outstanding balance exceeding your current vehicle's worth, wait to trade it in until you've paid it down to match its value. Starting your next loan with old debt creates a financial hole that's difficult to escape. You're financing money that provides zero transportation benefit.

Buy vehicles that hold their value. Some brands and models depreciate more slowly than others. Trucks, certain SUVs, and specific brands like Toyota and Honda typically retain value better than luxury sedans or electric vehicles. Research depreciation rates before buying.

Many drivers don't realize they're in a vulnerable position until it's too late. The combination of minimal down payments and extended loan terms creates a multi-year window where you're financially exposed. Gap insurance costs less than a single car payment but can save you thousands when the unexpected happens. It's one of the most overlooked yet valuable coverages available

— Rebecca Chen

Frequently Asked Questions

Discovering your car totaled still owe on loan creates immediate financial stress, but it's a solvable problem. Your loan obligation doesn't disappear with your vehicle—you're responsible for the full balance regardless of what insurance pays. The gap between actual cash value and loan payoff becomes your burden unless you have gap insurance.

Your options range from paying the deficiency immediately to negotiating with your lender for a settlement or payment plan. Challenge your insurance company's valuation if you believe it's too low. Whatever path you choose, act quickly and maintain communication with your lender to protect your credit and minimize additional costs.

Future car purchases should include gap insurance if you're putting down less than 20%, financing for longer than 60 months, or rolling negative equity into your loan. Larger down payments and shorter loan terms keep you from developing negative equity in the first place. Understanding these principles before you need them prevents financial crisis when accidents happen.

The worst response is ignoring the problem. Your lender won't forget the deficiency, and defaulting triggers consequences that follow you for years. Face the situation directly, explore all available options, and make the choice that fits your financial circumstances. Thousands of drivers successfully navigate this challenge every year—with the right information and approach, you can too.

Related Stories

Read more

Read more

The content on this website is provided for informational and educational purposes only. It offers general guidance on topics related to car loans, auto refinancing, interest rates, credit scores, loan terms, and vehicle financing options. The information presented should not be considered financial, legal, or professional advice.

Auto loan terms, interest rates, approval requirements, and refinancing options may vary depending on the lender, credit profile, and individual circumstances.

While we aim to keep the information accurate and up to date, we make no guarantees regarding its completeness or reliability. Visitors should review official loan documents and consult with qualified financial professionals before making decisions related to auto loans or refinancing.