New sedan buyer reviewing car loan and insurance documents at dealership

Gap Insurance for Car Loan Explained

Content

Content

Picture this: You buy a shiny new sedan for $32,000, make your first payment, and then—three months later—someone runs a red light and totals your car. Your insurance company cuts you a check for $26,000 (what the car's worth now), but you still owe $30,500 on your loan. Where does that $4,500 come from? Out of your pocket, unless you bought gap insurance.

Most car buyers either purchase this coverage without really understanding it, or they skip it entirely and hope nothing goes wrong. Both approaches miss the point. The real question isn't whether gap insurance exists—it's whether your specific situation creates enough risk to justify the cost.

Let's cut through the sales pitches and fine print to figure out if you actually need this protection.

What Is Gap Insurance on a Car Loan?

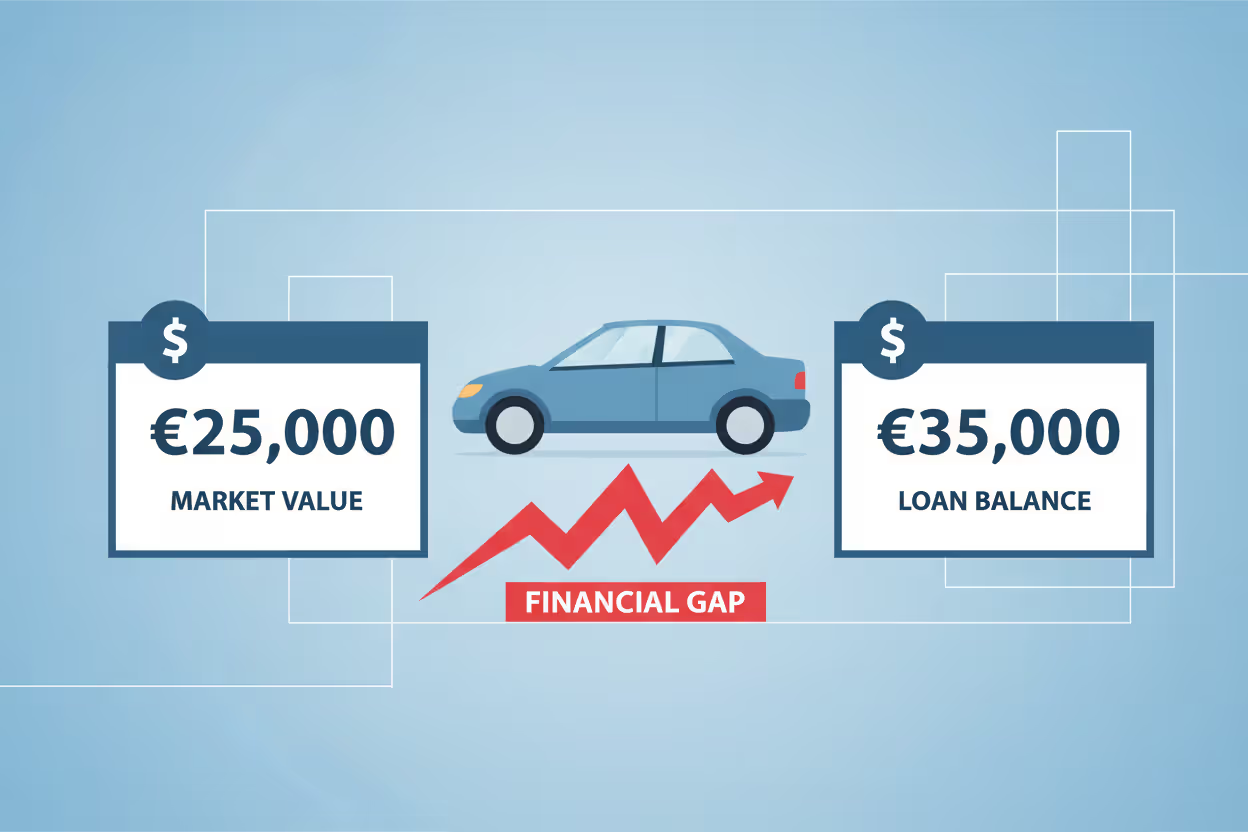

Think of gap insurance on car loan protection as a safety net for the difference between two numbers: what your car is actually worth versus what you still owe your lender. The "GAP" originally meant Guaranteed Asset Protection, but these days most people just call it gap coverage.

Your regular car insurance only cares about one thing: your vehicle's current market value (called "actual cash value" or ACV in insurance speak). Let's say you financed a $30,000 truck with minimal money down. Eight months later, someone steals it. Your insurance company determines it's now worth $24,000 due to depreciation. They'll pay you $24,000. Period.

Your auto lender? They want their $27,500 back—the full amount you still owe. That $3,500 gap doesn't magically disappear. Someone has to pay it, and without gap coverage, that someone is you.

This problem shows up most often when:

You put little or nothing down: Finance the entire purchase price (or more, if you had negative equity from your trade-in), and you're upside-down from minute one.

Your vehicle loses value quickly: Most new cars shed 20-30% of their value within twelve months. Some models—luxury sedans especially—drop even faster, sometimes hitting 35% depreciation in year one.

You chose a longer loan: Those 72-month and 84-month loans sound appealing because of lower payments, but your balance drops like molasses while your car's value drops like a rock.

What won't gap insurance car loan coverage handle? It won't touch your deductible. It won't cover missed payments or late fees. Extended warranties you rolled into the loan? Not covered. The coverage exists purely to address one specific problem: the depreciation gap between ACV and loan payoff.

Author: Brandon Ellsworth;

Source: ruralxchange.net

How Gap Insurance Works with Car Loans

Let me walk you through an actual scenario. Tom bought a $38,000 crossover SUV in February 2025. Put down $2,500, financed $35,500 at 7% over 72 months. Fast forward to October—ten months later—and he rear-ends someone on the highway. The damage is so extensive that his insurance company declares it a total loss.

Here's where things get interesting:

- Tom's remaining balance: $33,200

- Insurance valuation (ACV): $28,500

- His comprehensive deductible: $500

The insurance check comes out to $28,000 after subtracting his deductible. He still owes $33,200. That leaves a $5,200 gap sitting there like an unwanted houseguest. If Tom bought gap coverage, it handles that entire $5,200. Without it? He's writing a check from savings while also scrambling to find money for his next vehicle.

Here's the typical claims process:

- Your primary insurer totals the car and calculates its ACV

- You get their payout (ACV minus your deductible)

- You submit a gap claim with documentation showing what you owe

- The gap insurer contacts your lender to verify the payoff amount

- They send payment directly to your lender for the difference

Most claims wrap up within two to four weeks once you've submitted everything. The money never touches your hands—it goes straight to the lender to clear the debt.

Author: Brandon Ellsworth;

Source: ruralxchange.net

What gap insurance won't touch matters as much as what it covers:

- Past-due payments or any late charges

- Extended warranties or maintenance plans you financed

- Credit insurance or similar add-ons

- Leftover debt from your previous vehicle

- Your standard insurance deductible

- Claims for diminished value

- Rental car costs while shopping for a replacement

Some policies cap their payout at 25% of your car's ACV. If your gap exceeds that threshold, you're stuck covering the excess. Read the actual policy language before you buy—don't just trust what the salesperson tells you.

Do I Need Gap Insurance on a Car Loan?

The answer to "do I need gap insurance on a car loan" depends entirely on your loan structure and financial cushion. Gap coverage makes tremendous sense in these situations:

Your down payment was less than 20%: A skimpy down payment—say, 5% on a $28,000 purchase—puts you underwater immediately. Once depreciation kicks in, that gap widens fast.

You financed for longer than 60 months: Six-year and seven-year loans mean you're barely chipping away at the principal while depreciation does its thing. You'll stay upside-down for years.

Your vehicle depreciates aggressively: Certain luxury cars, some electric vehicles (depending on make and model), and specific brands lose value alarmingly fast. A car that drops 35% in year one creates a much bigger gap than average.

You rolled over negative equity: Had a trade-in where you still owed money? If the dealer folded that debt into your new loan, you started thousands of dollars behind before accounting for any depreciation.

You're leasing: Lease contracts almost always require gap protection, and lessors typically include it automatically.

Your emergency fund couldn't absorb a $6,000 surprise: If writing a check for five or six thousand dollars would seriously hurt you financially, gap insurance offers real protection.

You can probably skip gap coverage when:

- You put down 20% or more of the purchase price

- Your loan term is 48 months or shorter

- You're financing a vehicle known for holding its value well (certain trucks and SUVs, for example)

- You've got enough savings to cover a $5,000-$8,000 gap without stress

- Your current loan balance already sits below your car's market value

Check your loan-to-value ratio every six months or so. Most lenders show this in your online portal. Once you owe less than what your car is worth, the gap has closed and you can drop the coverage.

Author: Brandon Ellsworth;

Source: ruralxchange.net

Is Gap Insurance Worth It on a Car Loan?

Figuring out if gap insurance is worth it on a car loan means comparing what it costs against your actual exposure. The math shifts dramatically depending on where you purchase it and how large your gap truly is.

Through a dealership, expect to pay $400-$700 as a one-time charge rolled into your financing. Through your existing auto insurer, it typically runs $20-$40 annually. Over a five-year period, that's $100-$200 total versus potentially $700 from the dealer—and you're paying interest on that $700 for years.

Let's look at real numbers:

You finance $30,000 over 72 months after putting $2,000 down. Based on typical depreciation curves, your vehicle will probably be worth around $22,000 at the end of year one, while you'll still owe approximately $26,500. That's a $4,500 gap. Paying $60 for two years of coverage ($120 total) to protect against a potential $4,500 loss? That's sensible risk management. Paying $600 at the dealership for identical protection? Harder to justify, though still valuable if you're living paycheck-to-paycheck.

The coverage makes financial sense when:

Your gap risk peaks early: The first 18-24 months present the biggest danger zone. Depreciation hits hard while your loan balance barely budges.

You can't self-insure the risk: If a $5,000 surprise expense would wreck your budget, spending $100-$200 for protection is money well spent.

You're buying through your insurer: At $20-$40 per year, the cost is negligible compared to the potential loss.

You financed more than the vehicle's value: Starting significantly underwater increases the odds you'll actually need to file a claim.

Skip it when:

- You could comfortably cover a $6,000-$10,000 gap from your emergency fund

- You've already paid down enough principal to close the gap

- The dealership wants more than $400 (buy it elsewhere)

- Your combination of down payment and loan term creates minimal risk

Here's something many buyers overlook: certain comprehensive auto insurance policies now include "new car replacement" for vehicles under a year or two old. This essentially duplicates gap protection. Check your current policy before purchasing separate gap coverage.

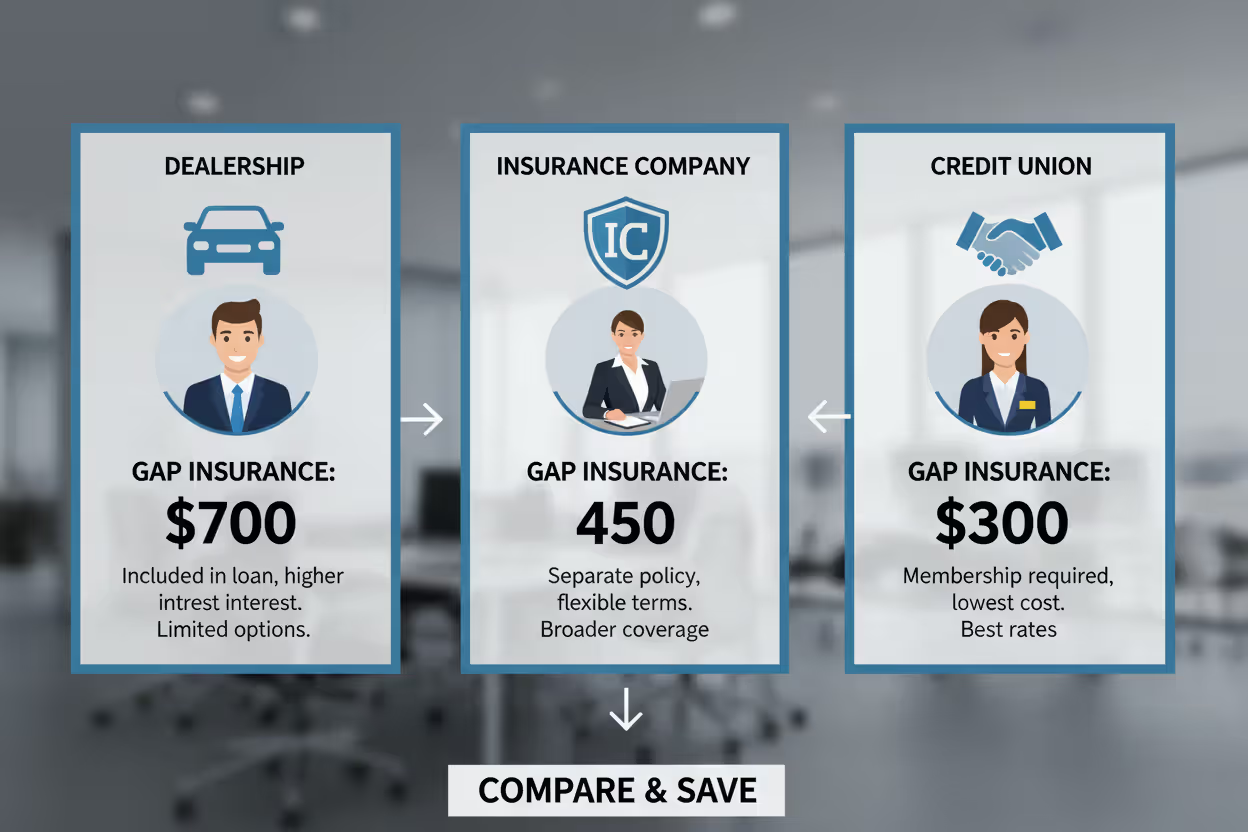

Where to Buy Car Loan Gap Insurance and What It Costs

You've got three main options for car loan gap insurance, each with different pricing and trade-offs.

| Provider Type | Average Cost | Coverage Caps | Cancellation & Refunds | Best Fit |

| Car Dealership | $400-$700 (one-time fee, financed) | Often limited to 25% of ACV | Pro-rated refund available but paperwork-heavy | Convenience seekers; buyers with limited insurance options |

| Auto Insurer | $20-$40/year (added to current policy) | Varies by carrier; frequently up to $50,000 | Cancel anytime; no refund but charges stop | Most drivers; simplest and cheapest option |

| Credit Union/Bank | $200-$400 (one-time) or $15-$30/year | Usually 25-30% of ACV | Pro-rated refunds typically offered | Members wanting competitive pricing from a trusted source |

Dealership gap insurance wins on convenience—you handle everything during the vehicle purchase. The massive downside? Cost. Dealers mark up gap coverage heavily, sometimes hitting $600-$700 for protection you could obtain elsewhere for under $200 over the same timeframe. Plus, since you're financing that premium, you'll pay interest on it throughout the loan.

Auto insurance companies offer the smartest value for most buyers. Tacking gap coverage onto your existing policy takes five minutes and costs about what you'd pay for a music streaming service. You can drop it anytime hassle-free, and you're not paying interest since nothing gets financed. The catch: you must carry comprehensive and collision coverage, and most insurers require you to add gap protection within 30 days of purchase (sometimes they'll allow up to 90 days).

Banks and credit unions split the difference. Financing through a credit union? They usually offer gap insurance at decent rates—better than dealers, occasionally slightly higher than major insurers. If you're already a member, the application process is straightforward.

Worth getting quotes from: State Farm, Progressive, Nationwide, and USAA (if you're military-affiliated). Grab quotes from at least two sources. The actual coverage terms rarely differ much between providers, making price the deciding factor.

Timing matters here. Most insurers require you to add coverage within 30 days of buying your vehicle, though some extend this to a year. Waiting doesn't save money with annual policies—you just go unprotected during your highest-risk window.

Author: Brandon Ellsworth;

Source: ruralxchange.net

How to Cancel Gap Insurance on Your Car Loan

Cancel gap insurance once you've built enough equity that your car's value exceeds your loan balance. Keeping it beyond that point wastes money, but dropping it prematurely leaves you exposed.

Watch for these milestones:

Your loan balance falls below your vehicle's worth: Pull up Kelley Blue Book or Edmunds every six months to estimate your car's value, then compare it against your payoff amount. Once you've got positive equity (owing less than the car is worth), gap coverage serves no purpose.

You pay off the loan completely: Gap insurance becomes instantly worthless when no loan exists. Cancel it the same day.

You refinance and significantly reduce your principal: A refi that drops your balance substantially might eliminate your gap entirely.

You sell or trade in the vehicle: Coverage ends automatically when you transfer ownership.

Most borrowers hit the equity milestone somewhere between 24-48 months, depending on their down payment, loan length, and depreciation rate. A vehicle with strong resale value combined with a shorter loan closes the gap much faster.

How you cancel depends on who sold you the coverage:

Insurance company policies: Call your insurer and request gap removal. Takes effect immediately or at your next renewal. You won't get money back on annual policies, but the charges stop.

Dealership or lender policies: Submit written cancellation to whoever sold the coverage (usually the finance company servicing your loan). You'll typically get a pro-rated refund based on unused time. If you financed the gap insurance cost, that refund usually applies to your loan principal rather than coming back to you as cash.

You'll usually need:

- Written cancellation request including your loan account number

- Current odometer reading

- Proof you've maintained required insurance

Refunds take anywhere from two to eight weeks to process. If you haven't heard anything in 30 days, follow up.

Important caveat: some dealership gap policies include "non-refundable" language or offer minimal refunds. This is yet another reason to avoid dealer gap coverage when possible. Ask about their refund terms before purchasing anything.

Common Gap Insurance Mistakes to Avoid

Author: Brandon Ellsworth;

Source: ruralxchange.net

Even financially savvy borrowers make expensive mistakes with gap insurance.

Accepting dealership pricing without comparison shopping: This is the most costly error. A $600 dealer policy versus $120 total through your auto insurer over three years equals $480 down the drain. Always get quotes from your insurance company before signing anything at the dealership. If the finance manager pressures you to decide on the spot, that's your signal to walk away from their gap offer. You can add coverage after finalizing your vehicle purchase.

Buying coverage when your situation doesn't warrant it: Salespeople earn commissions on gap insurance, motivating them to sell it to everyone who walks through the door. If you dropped 25% down on a 48-month loan for a Toyota Tacoma (known for stellar resale), you probably don't need gap coverage. Calculate your actual risk instead of accepting blanket recommendations.

Ignoring the exclusions and caps: Some policies max out at 25% of your vehicle's ACV. If your gap exceeds that percentage, you're covering the rest yourself. Others deny claims if you've missed loan payments. Know exactly which situations trigger payment and which don't.

Thinking gap insurance covers everything beyond the ACV: It won't pay your deductible, late charges, financed warranties, or rolled-over negative equity from your previous car. Many borrowers discover these exclusions only after filing a claim.

Maintaining coverage after the gap disappears: Paying for gap insurance once you've built positive equity throws money away. Check your loan balance against your car's value at least once a year, and cancel when you've crossed that threshold.

Purchasing duplicate coverage: Some comprehensive auto policies include new car replacement, which works similarly to gap insurance for newer vehicles. Verify you don't already have protection before buying a separate gap policy.

Missing the enrollment window: Most insurers require adding gap coverage within 30 days of vehicle purchase. Miss that window and you're stuck with pricier dealer or lender options—if they're even still available.

Forgetting to request your refund: If you financed gap insurance through the dealer and paid off your loan ahead of schedule, you're often entitled to a refund. Many borrowers never claim it because they don't know it exists.

The biggest mistake I see is treating gap insurance like an all-or-nothing choice. The smart play is purchasing it when you genuinely need it—usually the first two or three years of a loan with minimal down payment—then canceling once you've built equity. At $20-$40 annually through your auto insurer, the cost is negligible during your high-risk period, and you're not trapped paying for coverage you've outgrown

— Jennifer Martinez

Frequently Asked Questions

Gap insurance for car loan protection addresses a specific vulnerability: getting financially destroyed if your vehicle is totaled before you've built sufficient equity. Whether you need it hinges on your down payment size, loan duration, vehicle depreciation rate, and financial reserves.

The decision becomes straightforward once you run the numbers. Calculate your probable gap by comparing your loan balance trajectory against expected depreciation for your specific vehicle. If that gap could hit $4,000-$8,000 and you couldn't comfortably absorb that cost from savings, gap insurance makes sense—particularly at $20-$40 per year through your auto insurer.

Avoid the dealership markup whenever you can. Shop gap coverage with the same diligence you applied to shopping for your vehicle. Add it when your risk is real, cancel it when your situation changes, and never duplicate coverage you already carry.

The security gap insurance delivers during your loan's highest-risk window costs less than what most people spend on coffee monthly. For borrowers with small down payments and extended loan terms, that's a reasonable trade.

Related Stories

Read more

Read more

The content on this website is provided for informational and educational purposes only. It offers general guidance on topics related to car loans, auto refinancing, interest rates, credit scores, loan terms, and vehicle financing options. The information presented should not be considered financial, legal, or professional advice.

Auto loan terms, interest rates, approval requirements, and refinancing options may vary depending on the lender, credit profile, and individual circumstances.

While we aim to keep the information accurate and up to date, we make no guarantees regarding its completeness or reliability. Visitors should review official loan documents and consult with qualified financial professionals before making decisions related to auto loans or refinancing.