Concerned car owner reviewing auto loan documents beside a vehicle

How to Get Out of a Car Loan Without Ruining Your Credit

Thousands of drivers realize within months that their car loan was a mistake. Maybe that $65,000 truck made sense before inflation hit. Perhaps your income dropped after signing papers. Or you're simply drowning in a payment that eats 20% of your take-home pay.

Here's something most dealers won't tell you: you have options. Not easy ones, and certainly not free ones, but legitimate ways to escape without destroying your financial future. The trick? Understanding which strategy matches your specific situation—because picking wrong can cost you $10,000 or tank your credit score by 150 points.

Why People Want to Exit Their Car Loans Early

Walk into any bankruptcy attorney's office and you'll hear the same story. "I thought I could afford $850 a month." Then layoffs hit. Medical bills piled up. A spouse lost their job. What felt comfortable in January becomes impossible by June.

Recent Federal Reserve data shows Americans now owe over $1.6 trillion in auto debt. Monthly payments on new vehicles? They've climbed past $750 on average, with many buyers locked into $900+ payments for 72 or 84 months. That's longer than most people keep the car.

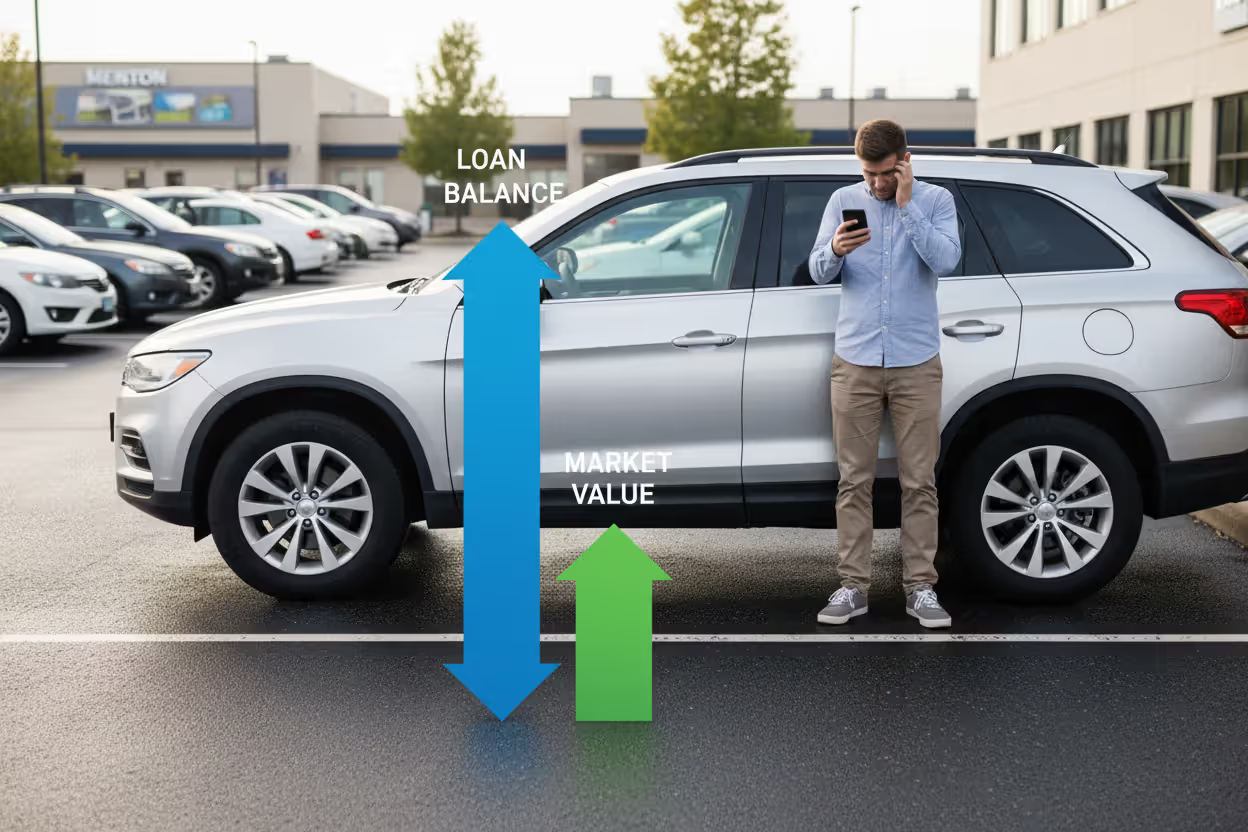

Then there's the negative equity trap. You drive your shiny new SUV off the lot, and it immediately loses 20% of its value. Put down $2,000, finance $45,000, and six months later you owe $42,000 on a vehicle worth $36,000. Congratulations—you're $6,000 underwater.

Author: Derek Halvorsen;

Source: ruralxchange.net

Dealerships love rolling every possible fee into your loan amount. Extended warranties you'll never use. Gap insurance you might not need. Nitrogen-filled tires. Paint protection. Suddenly your $38,000 car costs $44,000 financed, accelerating that negative equity nosedive.

Life doesn't care about your loan term either. You get divorced and can't afford the payment alone. Your family grows and that coupe becomes impractical. You commute 80 miles daily in a V8 truck and gas costs are murdering your budget. The reasons vary, but the financial pain is universal.

Can You Get Out of a Car Loan Legally?

Yes, but let's kill one myth immediately: your dealer doesn't have to take the car back. That "cooling off period" you've heard about? It doesn't exist in most states for vehicle purchases. Once you've signed and left the lot, you own it—and you owe the money.

Your loan contract is legally binding. You promised to repay the borrowed amount, plus interest, over an agreed timeline. The lender placed a lien on your title, meaning they technically own the car until you've paid every penny. They're not required to release you from that obligation just because you've changed your mind.

Different lenders operate under different policies, though. Credit unions often show more flexibility than big banks or captive auto finance companies. A borrower with perfect payment history for two years might find their credit union willing to work with them. Someone who's already 60 days late? Much harder conversation.

Your equity position matters enormously. Owe $15,000 on a car worth $20,000, and you've got leverage and options. Owe $30,000 on that same car? You'll need $10,000 cash to escape, or you'll be negotiating from a position of weakness.

Can you legally exit your car loan? Absolutely. Easily or cheaply? That depends entirely on your situation, and there's no universal answer. Anyone promising otherwise is selling you something.

Seven Ways to Get Out of a Car Loan

Author: Derek Halvorsen;

Source: ruralxchange.net

Sell the Car and Pay Off the Loan

Private party sales typically net you $2,000-$4,000 more than dealer trade-in values. List your car on Facebook Marketplace, Craigslist, or Autotrader. If the car's worth $22,000 and you owe $19,000, you'll pocket $3,000 after payoff.

But what if you're upside down? Say you owe $26,000 and the car's worth $21,000. You'll need $5,000 cash to complete the transaction. Many sellers don't realize this until they're negotiating with buyers and the math doesn't work.

Here's the process: Get your exact payoff amount from your lender (it includes per-diem interest, so it changes daily). Find a buyer. Meet at the buyer's bank if possible. The buyer's bank cuts a check to your lender for the payoff amount. You cover any shortfall. Your lender releases the title to the new owner.

Never—and I mean never—let someone drive off with your car before the loan is paid. Scammers will give you a fake cashier's check, take possession, and disappear. You're left with no car and a loan you still owe.

This approach works brilliantly if you have positive equity or savings to cover negative equity. Your credit stays clean because you've fulfilled the contract. The loan gets marked "paid as agreed," which actually helps your credit history.

Refinance With a Different Lender

Refinancing swaps your current loan for a new one, hopefully with better terms. Your $650 payment at 8.9% interest might drop to $525 at 5.9%. That $125 monthly savings could mean the difference between manageable and impossible.

You'll typically need credit scores around 650 or higher. Lenders also examine your loan-to-value ratio—if you owe $28,000 on a car worth $20,000, many won't touch it. They're not in the business of financing negative equity.

Here's the catch everyone misses: extending your 48-month remaining term to 72 months lowers your payment but costs you thousands in additional interest. You might pay $3,500 more over the life of the loan despite the lower monthly amount. You're not escaping the loan—you're making it more comfortable while paying more overall.

Shopping rates matters enormously. A credit union might offer 5.5% while an online lender wants 7.2%. On a $25,000 loan, that difference costs you around $2,000 over 60 months. Check at least three lenders before deciding.

Transfer the Loan to Another Buyer (Lease Assumption)

Loan assumptions are rarer than unicorns in the auto world, but some lenders permit them. You find someone willing to take over your payments and ownership. They qualify with the lender based on their credit and income. You walk away clean.

The new buyer must satisfy the lender's underwriting standards, which often mirror what you went through originally. They'll verify income, run credit, and assess debt-to-income ratios. If they don't qualify, the deal dies.

Lenders charge assumption fees ranging from $250 to $600. You'll also need to find someone willing to accept your existing interest rate and terms. If you're paying 9.5% interest and current market rates are 6%, good luck finding a qualified buyer willing to overpay by thousands.

Call your lender first. Ask specifically: "Do you allow loan assumptions on auto loans?" Most will say no. Some credit unions and smaller banks say yes under certain conditions. Don't waste weeks looking for a buyer if your lender prohibits transfers entirely.

Voluntary Surrender or Repossession

This option is a financial nuclear bomb. Use it only when you literally cannot make payments and have exhausted every other possibility.

Here's what happens: You contact your lender and arrange to return the vehicle. They send it to auction. Let's say you owed $24,000. The car sells for $16,000 at auction. You now owe the lender $8,000 plus their repossession costs (towing, storage, auction fees)—often another $1,200. Total deficiency: $9,200 that you still legally owe.

Your credit score will plummet 100-150 points immediately. That repossession mark sits on your credit report for seven full years from the date of your first missed payment. During that time, you'll struggle to get approved for credit cards, apartments, or mortgages. If you do get approved, expect subprime interest rates that cost you tens of thousands extra.

Voluntary surrender looks marginally better than involuntary repossession, where they send a tow truck at 3 AM to hook your car. But "marginally better" is like saying a broken arm is better than a broken leg. Both are terrible.

Some borrowers think surrendering eliminates the debt. Wrong. The lender can sue you for the deficiency balance. If they win (they usually do), they can garnish your wages or levy your bank account. Bankruptcy becomes the only escape.

Trade In Your Vehicle

Trading at a dealership offers maximum convenience and minimum value. The dealer appraises your car, offers you wholesale price (typically $2,000-$4,000 below private party value), and applies that toward your next purchase.

If you have positive equity, trading can work. Your $18,000 car with a $14,000 payoff gives you $4,000 toward the next vehicle. That's a solid down payment that lowers your new loan amount.

But here's where dealers trap desperate borrowers: they'll roll negative equity into your new loan. Owe $7,000 more than your trade is worth? They'll add that $7,000 to your next car's price. You're buying a $35,000 car but financing $42,000. You're underwater on day one of the new loan, and the cycle starts again—only worse.

I've seen buyers roll negative equity three times across three vehicles. They currently owe $48,000 on a $32,000 car and wonder why they can't refinance. This strategy works only when you're trading down significantly—like swapping a $600/month truck for a $350/month sedan. Otherwise, you're making your problem bigger.

Pay Off the Loan Early

Author: Derek Halvorsen;

Source: ruralxchange.net

Got a bonus? Inheritance? Lawsuit settlement? Paying off your loan completely is the cleanest exit. You own the car free and clear. Keep it, sell it, gift it—you're in control.

First, check your loan documents for prepayment penalties. Some lenders charge fees if you pay off early because they lose future interest income. These penalties are increasingly rare, but they exist, especially on subprime auto loans. A 2% penalty on a $30,000 payoff costs you $600.

Run the math before emptying your savings. If your loan is at 3.9% interest and you could invest that money at 8% returns, paying off the loan early actually costs you money. But if you're at 11.9% interest and barely have $2,000 in savings, paying it off eliminates a high-interest debt and the monthly payment burden.

This obviously requires significant cash—$15,000, $25,000, maybe more. Most people trying to escape car loans don't have that kind of money sitting around, making this option theoretical rather than practical.

Negotiate a Settlement With Your Lender

When you're severely delinquent—think 90+ days—and repossession is imminent, some lenders will accept less than the full balance. They've done the math: repossessing your car costs them money (towing, storage, auction fees), and the auction might only net them 60% of what you owe anyway.

You might owe $20,000 and offer them $14,000 to settle completely. They consider it. They're getting $14,000 guaranteed versus maybe $12,000 after repo costs and auction. Some lenders accept these settlements, especially if you can pay the lump sum immediately.

Understand the consequences. Your credit takes a massive hit—similar to repossession. The settled account appears on your credit report as "settled for less than full balance," which screams to future lenders that you defaulted. Expect your score to drop 120+ points.

And here's something most borrowers don't know: the IRS considers forgiven debt as taxable income. Lender forgives $6,000? The IRS treats that as $6,000 of income you must report on your tax return. At a 22% tax bracket, you'll owe $1,320 in additional taxes.

Lenders won't negotiate if you're current on payments. They only discuss settlements when you've already destroyed your credit by missing multiple payments. This isn't a strategic option—it's damage control when everything else has failed.

Best Way to Get Out of a Car Loan Based on Your Situation

Different circumstances demand different strategies. This breakdown helps you identify which path makes sense given your specific financial reality.

| Method | Credit Impact | Upfront Cost | Time Required | Best For |

| Sell the Car | No damage if paid completely | Moderate to high (covers any negative equity) | 2-8 weeks | Drivers with positive equity or enough savings to bridge the gap |

| Refinance | Minor (inquiry drops score 5-10 points) | Low (processing fees $100-300) | 2-4 weeks | People with improved credit wanting lower payments |

| Voluntary Surrender | Catastrophic (100-150 point drop) | Nothing upfront, but deficiency balance owed | 1-2 weeks | Absolute last resort when payments are impossible and no other option exists |

| Trade-In | Minimal if handled properly, moderate if rolling significant negative equity | High (especially with negative equity rolled into new loan) | 1-2 weeks | Buyers who need different vehicle immediately and have decent credit |

| Early Payoff | None (loan marked paid as agreed) | Very high (entire remaining balance) | 1 week | People with cash reserves from bonuses, inheritance, or savings |

| Loan Transfer | Minimal (doesn't reflect as refinance) | Low to moderate ($250-600 in fees) | 3-6 weeks | Borrowers who can locate qualified buyers and have lenders that permit assumptions |

| Settlement | Severe (similar to default/repossession) | Moderate (lump sum of 60-75% of balance) | 4-12 weeks | Borrowers already behind on payments facing imminent repossession who have lump sum available |

Match your available cash, credit situation, and urgency to the right method. Strong credit and positive equity open up nearly every option. Already behind on payments with no savings? You're choosing between bad options and worse options.

What Happens to Your Credit When You Exit a Car Loan

Your exit strategy determines whether your credit survives intact or craters for years.

Pay off your loan through a private sale or early payoff? Your credit might dip 5-15 points temporarily because you've closed an active installment account. Credit scoring models like seeing a mix of account types (credit cards, installments, mortgages). Close your only installment loan and you lose that diversity factor. But this dip recovers within months, and you avoid any negative marks.

Refinancing triggers what's called a hard inquiry—the lender pulls your credit report to evaluate your application. This typically drops your score 5-10 points. If you're shopping rates at multiple lenders within a 14-day window, credit bureaus count all those inquiries as a single event. Make timely payments on your new loan and your score recovers within 3-6 months, often higher than before as you build positive payment history.

Voluntary surrender annihilates your credit. Expect to lose 100-150 points immediately. The repossession notation remains visible for seven years from your first missed payment. During that time, traditional lenders won't touch you. Subprime lenders will, but they'll charge 18-24% interest rates. That $25,000 car loan at 22% costs you $15,000+ in interest over 72 months compared to $4,000 at 6%.

The deficiency balance your lender sends to collections adds another negative mark. Collections accounts can drop your score another 50-100 points. If the lender sues and wins a judgment, that judgment appears on your credit report and public records, compounding the damage.

Borrowers must thoroughly review their contract terms and understand every financial consequence before attempting to exit a car loan. What appears to be a quick solution today often creates credit complications that haunt them for the better part of a decade

— Michael Chen

Trading in with rolled negative equity doesn't immediately damage your credit, but it creates a dangerous situation. You're instantly underwater on the new loan, often by $5,000-$10,000. If your income drops or expenses increase, you're right back where you started, except now you owe even more.

Mistakes to Avoid When Trying to Get Out of a Car Loan

Ignoring your negative equity is the number one mistake. Borrowers assume they can just trade in or sell without doing basic math. Check your exact payoff amount (call your lender for the per-diem calculation). Then check your vehicle's current value on Kelley Blue Book, Edmunds, and NADA Guides. Use the "private party" value if selling yourself, "trade-in" value if going to a dealer. The difference between those numbers is reality—either cash in your pocket or cash you must bring to close the deal.

Stopping payments while you "figure things out" is financial suicide. Every missed payment drops your credit score 90-110 points. That missed payment stays on your credit report for seven years. If you're planning to sell your car next month, keep making payments this month. Destroying your credit to save $600 makes zero sense.

Loan assumption scams cost thousands of victims annually. Here's how it works: someone contacts you about "taking over your payments." They seem legitimate. They make two or three payments while driving your car. Then they stop paying and disappear. You're still legally responsible for the loan. The car is gone. Your credit is destroyed. And the lender is demanding $20,000. Always, always get lender approval in writing before allowing anyone to assume your loan. Better yet, use a title transfer service that handles the paperwork legally.

Refinancing without calculating true costs burns borrowers constantly. Your payment drops from $625 to $475—awesome, right? Except you extended your loan from 36 months remaining to 72 months. You're now paying $34,200 total instead of $22,500. That lower monthly payment just cost you $11,700. Run amortization calculators. Compare total interest paid, not just monthly payments.

Taking the first trade-in offer without shopping around leaves thousands on the table. Dealers low-ball initial offers because most customers accept them. Get written offers from three dealerships. Better yet, get a private party quote from Carvana, Vroom, or CarMax. These online buyers often beat local dealer offers by $1,500-$3,000. Use that higher offer as leverage when negotiating with traditional dealers.

Making deals over the phone without written confirmation creates he-said-she-said disasters. Your lender agrees to defer two payments while you sell the car. You stop paying. Sixty days later they're calling about your delinquency, and suddenly no one remembers your agreement. Every arrangement must be in writing. Email confirmations work. Recorded calls work (in single-party consent states). Verbal promises with "David from the loan department" are worthless.

Author: Derek Halvorsen;

Source: ruralxchange.net

Frequently Asked Questions About Getting Out of Car Loans

Escaping a problematic car loan requires honest assessment of your financial reality and strategic selection of the exit method that minimizes long-term consequences. Borrowers with positive equity or solid credit scores can navigate this relatively painlessly through private sales or refinancing. Those facing negative equity or severe financial hardship must weigh the credit devastation of various options against their immediate need for relief.

Act quickly once you recognize you need out. Every month you wait, interest accumulates, your vehicle depreciates further, and negative equity grows. Missing payments while you deliberate destroys credit and eliminates options that require good standing with your lender.

After resolving your car loan situation, spend time understanding what went wrong. Did you buy more vehicle than you could afford? Accept a predatory interest rate? Put nothing down and finance every add-on? Make a larger down payment on your next vehicle—aim for 20% minimum. Choose shorter loan terms (48-60 months maximum). Ensure your monthly payment (including insurance and estimated maintenance) stays below 10-15% of your gross monthly income.

Credit recovery takes time but happens with consistent positive behavior. Even borrowers who've experienced repossession can rebuild scores within 2-4 years through on-time payments on other accounts. Add yourself as an authorized user on a family member's old credit card with perfect payment history. Get a secured credit card and use it responsibly. Pay everything on time, every time.

The lesson here? Getting into a car loan takes one afternoon at a dealership. Getting out takes weeks or months, often costs thousands, and sometimes damages your credit for years. Choose carefully the first time, and you'll never need to execute an emergency escape plan.

Related Stories

Read more

Read more

The content on this website is provided for informational and educational purposes only. It offers general guidance on topics related to car loans, auto refinancing, interest rates, credit scores, loan terms, and vehicle financing options. The information presented should not be considered financial, legal, or professional advice.

Auto loan terms, interest rates, approval requirements, and refinancing options may vary depending on the lender, credit profile, and individual circumstances.

While we aim to keep the information accurate and up to date, we make no guarantees regarding its completeness or reliability. Visitors should review official loan documents and consult with qualified financial professionals before making decisions related to auto loans or refinancing.