Car buyer reviewing auto loan documents and credit score before financing

Car Loan Rates by Credit Score Guide

Content

Content

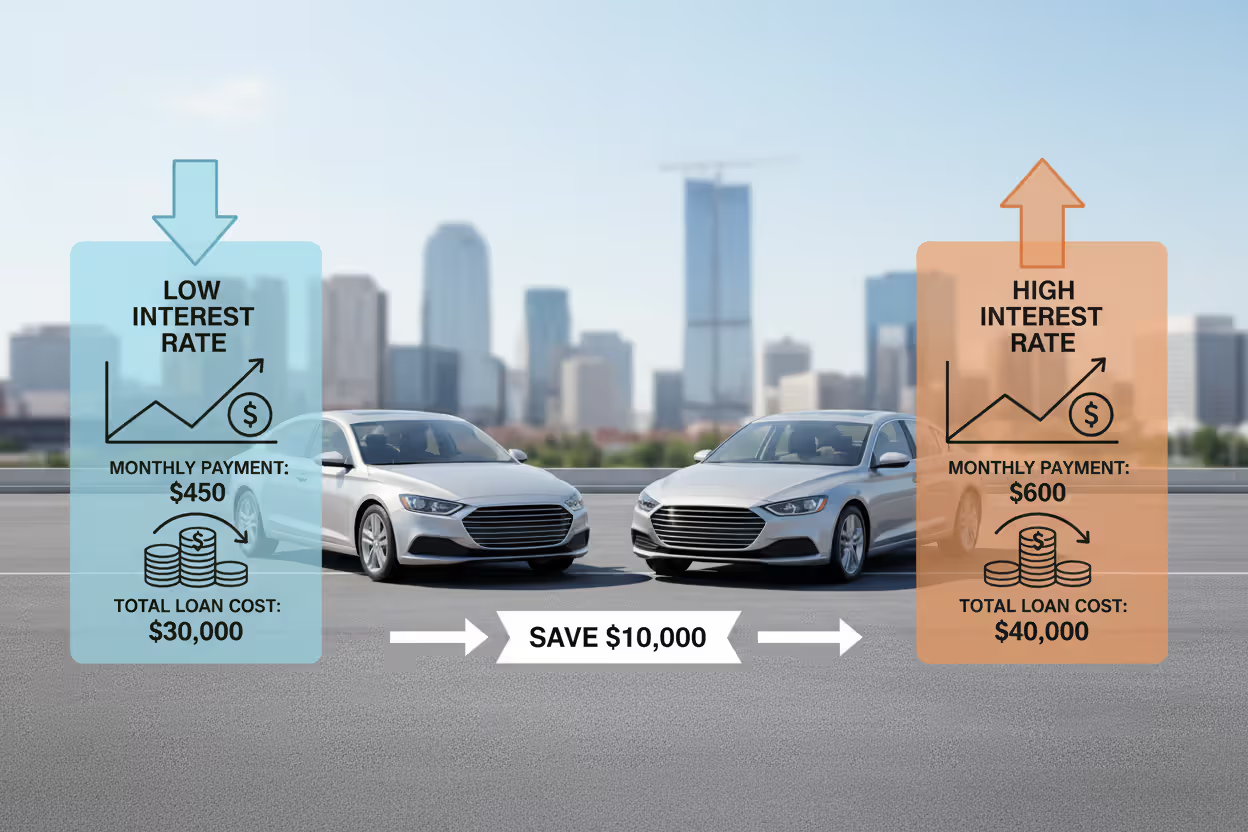

Here's something most car buyers learn the hard way: your credit score doesn't just nudge your interest rate slightly—it can literally double or triple what you'll pay. I'm talking about the difference between a 5% APR and an 18% APR on the exact same Toyota Camry. That seemingly small percentage gap? It'll cost you $6,000+ over the life of a typical loan.

This number hanging over your financial life—sitting somewhere between 300 and 850—basically determines whether financing a car makes sense or becomes a money pit. Auto lenders have been using credit scores since the 1990s for one simple reason: they're scarily accurate at predicting who'll actually make their payments. Someone with a 790 score defaults about once in every 200 loans. Someone with a 570? More like once in every 25 loans. Banks aren't being mean when they charge different rates—they're just doing math on their risk.

Understanding how this system works puts real money back in your pocket. You'll know what rates you should actually expect, which lenders are worth your time, and what you can do right now to save thousands before you ever set foot in a dealership.

How Credit Scores Affect Car Loan Interest Rates

Auto lenders live and breathe something called risk-based pricing. Basically, the riskier you look on paper, the more you pay to borrow money. Makes sense when you think about it—would you lend $25,000 to someone with a history of late payments at the same rate as someone who's never missed a bill?

The FICO Auto Score takes your regular credit score and tweaks it specifically for car loans. It actually looks harder at your history with previous auto loans and installment payments than it does at your credit card behavior. Had a car repo five years ago? That'll hurt you more than maxing out a Visa.

When your application lands on a loan officer's desk, you're getting dropped into one of five buckets: super prime, prime, near prime, subprime, or deep subprime. Each bucket has its own rate range. Right now in 2026, super prime folks (781-850 scores) are seeing offers around 5.8-7.2%. Down at the other end, deep subprime applicants (300-500) are getting quoted 19-21% or even higher.

Let me put actual dollars on this. Take a $30,000 loan for 60 months. At 6%, you'll pay about $580/month. At 15%, that jumps to $714/month. Over five years, that's an extra $8,000 flying out of your wallet—just because of your credit score. That's a used Honda Civic worth of money.

Author: Samantha Whitaker;

Source: ruralxchange.net

Lenders will tell you they're just covering their losses. And honestly, the data backs them up. Subprime borrowers default at rates 5-8 times higher than prime borrowers. When one in six loans goes bad instead of one in fifty, banks need to charge more on the good loans to stay in business.

Your credit score isn't just about whether you pay bills on time (though that's 35% of the calculation). It's also tracking how much you owe compared to your limits (30%), how long you've had credit (15%), new accounts you've opened recently (10%), and whether you have a mix of different credit types (10%). Someone who's been responsibly using credit for 15 years looks completely different than someone who just opened three credit cards last month—even if both have the same score.

Current Car Loan Interest Rates by Credit Score Range

Interest rates shift constantly based on what the Federal Reserve's doing, inflation, and how aggressively lenders are competing for business. But the spread between credit tiers? That stays pretty consistent. Here's what borrowers are actually seeing in early 2026.

New Car Loan Rates

Super prime buyers (781-850) are getting quoted 5.8-7.2% APR from banks, credit unions, and manufacturer financing arms like Toyota Financial or GM Financial. Prime borrowers (661-780) are looking at 7.5-10.1%. Near prime folks (601-660) are seeing 10.5-14.2%. Subprime territory (501-600) means 14.5-18.9%. Deep subprime (under 500)? You're probably looking at 19%+ unless you find a really generous credit union.

Now, there's a wrinkle here. Sometimes Toyota Financial or Ford Credit will run a promotion offering 2.9% or even 0% APR to move specific models. But there's always a catch—you need excellent credit, and the deal only applies to certain trim levels or last year's models sitting on the lot. Plus, taking the low rate usually means you can't combine it with rebates, which might be worth more.

Used Car Loan Rates

Used car financing costs more across the board—usually 1-2 percentage points higher than new cars. Why? Older vehicles break down more, they're harder to resell after repossession, and they lose value faster.

Super prime applicants are paying 7.1-9.3% on used cars. Prime borrowers see 9.8-12.5%. Near prime candidates get quoted 13.1-16.8%. Subprime rates land between 17.2-21.4%. Deep subprime? We're talking 22%+ pretty regularly.

The car itself matters too. A three-year-old certified pre-owned BMW from a dealer might qualify for rates close to new car pricing. But a 12-year-old Chevy with 140,000 miles? Expect to add another 2-4 percentage points regardless of your credit score. Banks hate lending on old, high-mileage cars because they're worth nothing after repossession.

Average Car Loan Interest Rates by Credit Score Range (2026)

| Credit Score | Category | New Car APR | Used Car APR | Monthly Payment (New, $30K/60mo) | Monthly Payment (Used, $30K/60mo) |

| 781-850 | Super Prime | 5.8-7.2% | 7.1-9.3% | $578-$596 | $596-$628 |

| 661-780 | Prime | 7.5-10.1% | 9.8-12.5% | $600-$639 | $631-$672 |

| 601-660 | Near Prime | 10.5-14.2% | 13.1-16.8% | $644-$698 | $681-$740 |

| 501-600 | Subprime | 14.5-18.9% | 17.2-21.4% | $702-$769 | $746-$822 |

| 300-500 | Deep Subprime | 19.2-21.5% | 22.1-24.3% | $775-$809 | $825-$862 |

These numbers assume you're financing $30,000 over 60 months at the midpoint rate for each range. Your actual rate depends on the specific lender, which car you're buying, and your complete financial picture.

What Determines Your Car Loan Interest Rate

Your credit score is huge, but it's not the only thing lenders care about. Several other factors can push your rate up or down by a full percentage point or more.

How long you're borrowing for makes a bigger difference than most people realize. A 36-month loan almost always gets you a lower rate than a 72-month loan—we're talking 0.5-1.5 percentage points lower. Lenders prefer shorter loans because their money's at risk for less time. The downside? Your monthly payment goes up. But you'll save thousands in interest.

Your down payment directly cuts the lender's risk. Put down 20% or more, and you'll often shave 0.25-0.75 points off your rate. Finance the whole purchase price—especially on a used car—and expect your rate to go up. Banks really hate when you owe more than the car's worth from day one (called being "underwater"), because if you default, they lose money even after selling the repossessed vehicle.

Your debt-to-income ratio compares all your monthly debt payments to your gross monthly income. Most mainstream lenders want to see this under 40-45%. Some subprime shops will go up to 50%, but you'll pay for it. A high DTI tells lenders you're stretched thin financially—one unexpected expense and you might miss a car payment. That risk can add 0.5-1 percentage point to your quoted rate even with a decent credit score.

What you're buying affects your rate more than you'd think. Cars older than 7-8 years typically trigger rate increases of 2-4 percentage points. Salvage titles? Good luck finding a lender at all, and if you do, expect subprime rates regardless of your credit. Some luxury brands (Mercedes, BMW) sometimes get slightly better rates because they hold their value, while heavily modified vehicles or commercial trucks often face rate penalties.

Who you borrow from can make a huge difference. Credit unions consistently beat banks by 0.5-1.5 percentage points because they're not trying to maximize profits. Online lenders like LightStream or MyAutoloan compete aggressively on rates but might be pickier about who they approve. Dealer financing can be great when manufacturers are subsidizing rates, but dealers routinely mark up the rate they're approved for (called "rate markup") to pocket the difference as extra commission.

Author: Samantha Whitaker;

Source: ruralxchange.net

Car Loan Rates with a 600 Credit Score

A 600 credit score puts you right on the border—some lenders will treat you as near prime, others will slot you into subprime. It's not a great position, but it's not hopeless either.

Expect rate quotes between 12-16% for a new car, and 17-20% for used. Yeah, those rates sting. On a $25,000 loan for 60 months at 14%, you're looking at $581/month with nearly $10,000 in interest charges over the life of the loan. But here's the thing—that's still way better than deep subprime territory where rates can hit 24%.

Who'll actually approve you? Credit unions are your best bet, hands down. Many have special programs for members working to rebuild credit. Online lenders like Upstart or LendingClub use broader underwriting criteria—they'll look at your education, job history, and income patterns, not just your credit score. Sometimes they'll surprise you with a rate a couple points better than expected.

Subprime specialists like Credit Acceptance Corporation or Santander Consumer USA will definitely approve you, but their starting rates usually begin around 15% and go up from there. If you're financing through a dealer who uses these lenders, you're probably getting charged 16-20% because of dealer markup. Getting pre-approved directly cuts out that markup.

Here's what I'd actually do with a 600 score: wait. Seriously. Three to six months of focused credit improvement can bump you to 650 or even 680. That could drop your rate by 2-4 percentage points, saving you $3,000-$5,000 over a five-year loan. Pay down your credit cards to under 30% utilization (under 10% is even better). Pull your credit reports from all three bureaus and dispute any errors. Don't open any new accounts. Make every payment on time.

I see borrowers with 600 credit scores rush into car loans all the time, and it kills me. Three months of patience—paying down revolving debt and cleaning up credit report errors—can move them from subprime to near prime status. That's the difference between a 16% rate and an 11% rate. On a typical loan, that's $3,000-$4,000 in savings. Show me another investment that returns that much money in 90 days

— Michael Chen

How to Get Better Car Loan Rates with Your Credit Score

You can't change your credit score overnight, but you can absolutely work the system to get better rates than you'd otherwise qualify for. Here's how.

Fix your credit before you apply. Get your free credit reports from AnnualCreditReport.com (all three bureaus) and look for mistakes. Found a collection account that's not yours? Dispute it. Seeing a late payment you actually made on time? Challenge it with documentation. Pay down credit card balances—get them under 30% of your limits, ideally under 10%. Don't close old accounts even if you're not using them; that hurts your average account age and your total available credit. Set up autopay on everything so you don't miss payments in the months before you apply.

Shop around like your financial life depends on it. Because it does. FICO treats multiple auto loan applications within 14-45 days as a single inquiry for scoring purposes, so you won't wreck your credit by rate shopping. Get quotes from at least one credit union (join one if you have to—it's worth it), one traditional bank, one online lender, and then compare against dealer financing. Credit unions beat competitors by 0.5-1.5 points so often that skipping them is just leaving money on the table.

Author: Samantha Whitaker;

Source: ruralxchange.net

Consider a co-signer if you've got someone willing. Adding your parents, a spouse, or a trusted friend with great credit can unlock prime rates even if your score is subprime. The co-signer is equally responsible for the debt—if you stop paying, they're on the hook—so this requires real trust. Some people use a co-signer to get a good initial rate, then refinance solo after 12-18 months of on-time payments.

Put more money down. Every extra dollar you put down reduces the lender's risk and improves your loan-to-value ratio. Many lenders have rate tiers based on LTV thresholds. Financing 95-100%? That's their highest rate bucket. Get down to 85-90%, and you might drop a tier. Below 80%? That's often the best rate tier. Sometimes an extra $1,500-$2,000 down can cut your rate by half a percentage point, which pays for itself in interest savings within the first couple years.

Choose a shorter loan term. A 48-month loan typically costs 0.5-1.0 percentage points less than a 72-month loan. Yeah, your monthly payment goes up, but your total interest paid drops dramatically. Run the numbers on both—sometimes the monthly payment difference is only $50-75, making the shorter term a no-brainer.

Mistakes That Increase Your Car Loan Interest Rate

People throw away thousands of dollars on avoidable mistakes. Don't be one of them.

Walking into a dealer without knowing your credit situation. You're negotiating blind. The dealer might tell you your credit's worse than it is to justify a higher rate. Or you might discover errors on your credit report only after getting a rejection. Pull your credit reports and check your scores 30-60 days before you start shopping. If there are problems, you've got time to fix them.

Taking dealer financing without shopping around first. Dealers mark up rates as standard practice—adding one or two percentage points on top of what the bank actually approved. The bank might've approved you at 8%, but the dealer quotes you 9.5% and pockets the difference. Getting pre-approved from your own bank or credit union gives you a comparison point and negotiating leverage.

Stretching to 72 or 84 months to afford a nicer car. This is how people end up paying $40,000 for a $30,000 car. Yes, a longer loan lowers your monthly payment. It also means you'll spend years underwater (owing more than the car's worth), and you'll pay double the interest. If you can only afford a car by stretching to 84 months, you're buying too much car. Period.

Skipping the pre-approval process. Getting pre-approved before you shop tells you exactly what you qualify for and at what rate. This knowledge keeps dealers from playing games with the numbers. It also speeds up the buying process and removes the pressure to accept whatever financing the dealer arranges because you've already got a backup option.

Focusing only on monthly payment instead of total cost. This is the #1 trick dealers use to sell you expensive financing. They'll ask "what monthly payment works for your budget?" then make that number happen by extending the loan to 84 months, bumping the interest rate, or both. Always calculate the total interest you'll pay—the difference between what you borrowed and what you'll actually pay back. That's the real cost of the loan.

Author: Samantha Whitaker;

Source: ruralxchange.net

Frequently Asked Questions About Car Loan Rates and Credit Scores

Your credit score controls what you'll pay to borrow money for a car—we're talking about differences of 10+ percentage points between excellent credit and poor credit. That translates to thousands of dollars over the life of a typical loan.

Before you start shopping for a car loan, pull your credit reports and fix any errors. Pay down credit cards to improve your utilization ratio. Then compare quotes from multiple lenders—at minimum a credit union, a bank, and an online lender—within a two-week window so it doesn't hammer your credit score. Even if your credit isn't great, shopping around makes a real difference.

If you're sitting around 600 or below, seriously consider waiting three to six months to improve your score. Getting from 600 to 650 could save you $3,000-$5,000 in interest. That's worth delaying your purchase unless you absolutely need a car immediately.

Getting a good rate isn't about luck or having connections. It's about understanding how the system works, preparing your credit profile, and shopping smart. Whether you've got an 800 score or you're rebuilding from 580, knowing the connection between credit scores and car loan rates helps you avoid expensive mistakes and keeps more money in your pocket where it belongs.

Related Stories

Read more

Read more

The content on this website is provided for informational and educational purposes only. It offers general guidance on topics related to car loans, auto refinancing, interest rates, credit scores, loan terms, and vehicle financing options. The information presented should not be considered financial, legal, or professional advice.

Auto loan terms, interest rates, approval requirements, and refinancing options may vary depending on the lender, credit profile, and individual circumstances.

While we aim to keep the information accurate and up to date, we make no guarantees regarding its completeness or reliability. Visitors should review official loan documents and consult with qualified financial professionals before making decisions related to auto loans or refinancing.