Buyer reviewing a used car loan contract with keys, calculator, and credit score chart

Average Used Car Loan Interest Rate by Credit Score

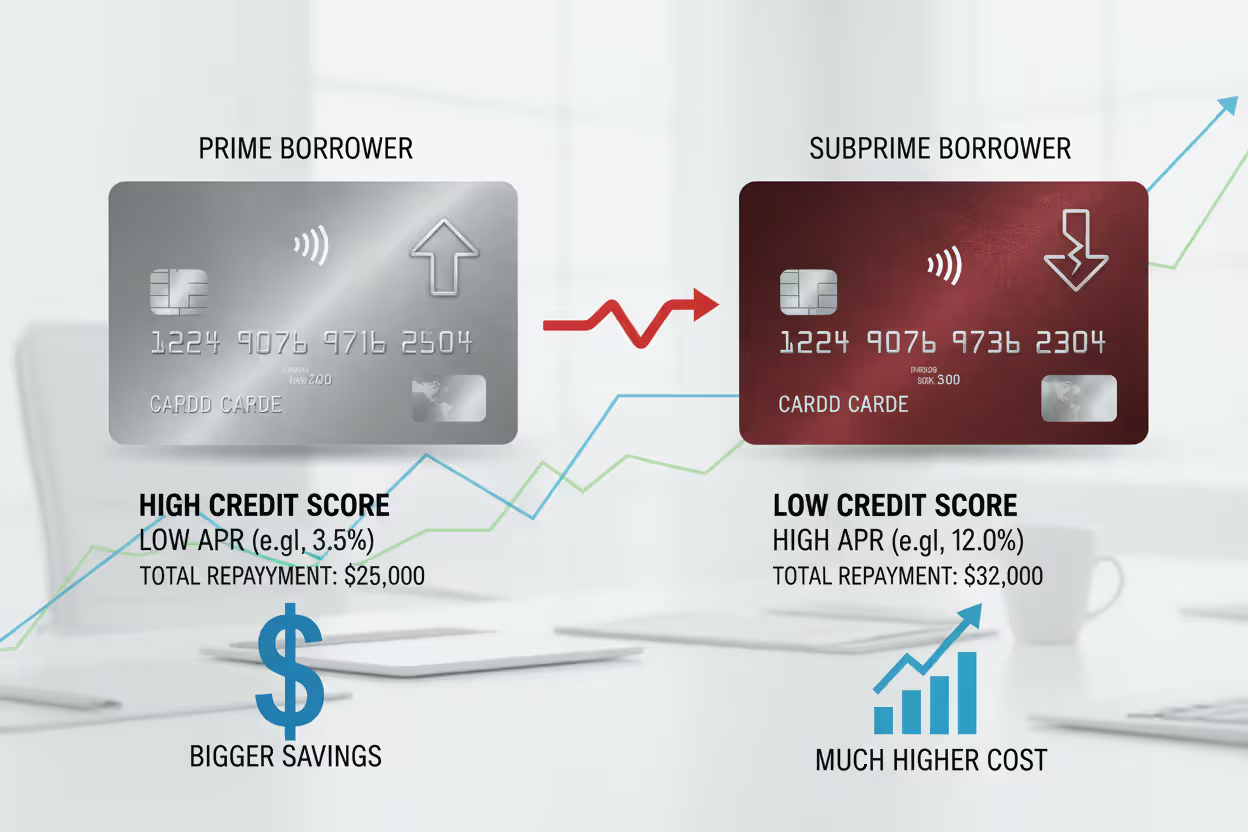

Your credit score determines what you'll actually pay for that used Honda Accord or Ford F-150—sometimes more than the negotiated price matters. While dealerships advertise monthly payments, the interest rate buried in your contract decides whether you're paying $22,000 or $29,000 for the same $20,000 vehicle.

Here's the brutal math: Someone with a 780 FICO score walks away with a 6.5% APR. Another buyer at 580? They're looking at 18% or higher. Both finance $25,000 over five years. The first pays around $3,800 in interest. The second? North of $10,600. That's $6,800 extra—enough for a solid down payment on their next car.

Most buyers don't realize lenders price risk this aggressively until they're sitting across from a finance manager. Knowing what rates match your credit profile before you shop prevents signing contracts you'll regret for the next five years.

What Determines Used Car Auto Loan Interest Rates

Your final APR comes from lenders weighing six major risk factors. Think of it like insurance underwriting—each element either raises red flags or earns you discounts.

Author: Derek Halvorsen;

Source: ruralxchange.net

Credit score dominates everything else. Banks pull your FICO Auto Score (not the same number you see on Credit Karma, by the way). This version emphasizes how you've handled past car loans and other installment debt. One 30-day-late payment from last year? Expect your rate jumping 2-3 points higher. Spotless payment history going back seven years? You've earned their best pricing.

Loan term works backward from what you'd expect. Want 72 or 84 months to shrink that monthly payment? Lenders tack on an extra 0.5-1.5 percentage points because you're borrowing their money longer. Default risk compounds over time. Choose 36 or 48 months instead, and you'll qualify for noticeably lower rates—though your monthly obligation climbs.

Vehicle age and condition matter more in used car lending than most people realize. Try financing a 2015 Camry with 90,000 miles versus a 2021 model with 28,000. Same buyer, same credit score. That older car triggers rate increases around 1-2 percentage points. Why? Lenders know older vehicles break down more often, and they depreciate faster. A major repair bill might tempt you to stop paying and walk away.

Down payment size signals commitment. Put down 20% or more, and you're telling the lender you won't abandon this loan when transmission problems hit. That confidence earns you 0.5-1 point lower rates compared to borrowers scraping together the minimum. Banks also recognize that larger equity stakes reduce their loss if they repossess.

Lender type creates wild rate swings. Credit unions typically beat traditional banks by 1-2 full percentage points for identical borrowers. Dealer financing introduces another wrinkle—markup. The dealer's lending partner might approve you at 7.5%, but the dealer quotes 9.5% and pockets the difference. That 2-point spread is negotiable, though most buyers never ask.

Debt-to-income ratio serves as the backup filter. Even with a 740 credit score, carrying a DTI above 43% raises concerns. Lenders worry you're stretched thin financially. They'll either decline you outright or add 1-2 percentage points to cover the perceived risk. The calculation? Add your monthly debts (car payment, student loans, credit cards, mortgage) and divide by your gross monthly income.

Each factor compounds. Strong credit with weak DTI might land you mid-tier pricing. Average credit with a large down payment could beat that. Lenders evaluate the complete picture when determining what the average interest rate for used car loan applicants becomes in your specific case.

Author: Derek Halvorsen;

Source: ruralxchange.net

Current Used Car Interest Rate Average in 2026

Used car auto loan interest rates have settled into a new normal after the chaos of 2022-2024. The Fed's monetary tightening finally plateaued through 2025, leaving us with a market where borrowers with excellent credit see rates around 6-7%, while those rebuilding credit face double digits.

Here's the breakdown across credit tiers right now:

| Credit Score Range | Average APR Range | Monthly Payment on $25K/60 Months |

| 781-850 (Super Prime) | 6.2% - 7.1% | $484 - $496 |

| 661-780 (Prime) | 8.3% - 10.2% | $509 - $533 |

| 601-660 (Near Prime) | 12.1% - 15.4% | $557 - $595 |

| 501-600 (Subprime) | 16.8% - 19.3% | $623 - $654 |

| 300-500 (Deep Subprime) | 20.2% - 24.1% | $667 - $709 |

These numbers blend all lender types and loan terms. Your actual quote swings based on those additional factors we just covered.

The used car interest rate average compressed a bit for prime and super prime borrowers in early 2026. More competition. Subprime rates? Still punishing, mostly because default rates in that segment spiked during 2024-2025 when inflation squeezed household budgets.

Geography matters too. Shop for a loan in California, Texas, or Florida, and you'll typically find rates 0.3-0.8 points lower than borrowers in states with fewer banking options. Credit union density drives this—states where more people bank at credit unions show better overall pricing.

We're watching a split market develop. Borrowers above 720 can actually negotiate and walk away from bad offers. Anyone below 640 faces take-it-or-leave-it terms from most lenders. The spread between best and worst rates hasn't been this wide since the 2008 financial crisis. If you're planning to buy in the next year, improving your credit score returns more value than any other single action

— Jennifer Hartmann

How Used Car Rates Compare to New Car Rates

Used car loans cost more. Always. Typically 2-4 percentage points more across every credit category. That same borrower qualifying for 4.9% on a 2026 model gets quoted 7.5% on a three-year-old version.

Why? Manufacturers subsidize new car financing through their captive lenders—Toyota Financial, GM Financial, Ford Credit. They're motivated to clear inventory and build brand loyalty. Those promotional rates you see advertised at 0.9% or 2.9%? Marketing expenses, essentially. No manufacturer backs used inventory once it's sold, so those incentives evaporate.

Depreciation creates the other problem. New cars follow predictable value curves for the first few years. Used cars? Their worth depends on accident history, maintenance records, previous owners, regional demand shifts. Lenders can't price that uncertainty precisely, so they build in cushion through higher rates.

Default patterns reinforce this pricing. Used car loans see higher default rates—partly because used car buyers average lower credit scores, but also because older vehicles need more repairs. A $2,500 transmission failure might push a tight-budget household into missed payments.

The average APR on used car loan contracts reflects all this compounded risk. Even certified pre-owned programs, which include manufacturer warranties and multi-point inspections, rarely match new car promotional rates.

Author: Derek Halvorsen;

Source: ruralxchange.net

One exception worth noting: Credit unions sometimes price their used car loans within a point of new car rates for top-tier members, especially on newer used inventory (1-3 years old). They're willing to sacrifice some margin to serve members. Worth checking if you qualify for membership.

Where to Find the Lowest APR on Used Car Loans

Where you apply matters as much as your credit score. Same borrower, same car, different lenders—rate quotes can vary by 3+ percentage points.

Credit unions consistently offer the best pricing. Their nonprofit structure means no shareholders demanding maximum returns. Those savings pass to members through lower loan rates—typically 1-2 points below commercial banks. Navy Federal, PenFed, Alliant—they're regularly quoting prime borrowers in the 6-8% range for used vehicles. Membership requirements have loosened considerably. Sometimes opening a savings account with $5 gets you in.

The downside? Slower approvals, and some won't finance vehicles over seven years old or past 100,000 miles. If you're buying a 2015 Civic with 110k on the odometer, some credit unions will decline regardless of your credit score.

Community and regional banks split the difference. They price about 0.5-1.5 points above credit unions but below national banks. The advantage shows up if you've banked there for years. That existing relationship—your checking account, maybe a mortgage—can override what your credit score alone suggests. Underwriters have more flexibility for known customers.

National banks (Chase, Bank of America, Wells Fargo) offer convenience and speed. Same-day digital approvals. Easy integration if you already bank there. But they rarely compete on price. Expect rates 1-2 points higher than credit unions for equivalent credit profiles. You're paying for convenience.

Online lenders disrupted this space recently. LightStream, AutoPay, myAutoloan—they've built tech-first platforms with competitive pricing. LightStream advertises used car rates starting at 6.99% for well-qualified borrowers and promises to beat any competitor's rate by 0.10 points. The catch? Selective underwriting. They want 700+ credit scores and stable employment history. If you qualify, they're fast and cheap.

Dealer financing means one-stop shopping but requires vigilance. Dealers don't lend their own money—they arrange financing through partner banks and credit unions. The dealer's lending partner might approve you at 7.5%, but the dealer quotes you 9.5%. That 2-point markup becomes dealer profit. Here's what most buyers miss: that markup is negotiable. You can bargain on the interest rate exactly like you negotiate the vehicle price.

The average APR used car loan shoppers actually accept typically runs 1-2 points higher than the best available rate simply because they didn't compare. Collect 3-4 quotes before you start shopping for vehicles. That preparation puts you in control.

Author: Derek Halvorsen;

Source: ruralxchange.net

How to Lower Your Used Car Loan Interest Rate

You're not stuck with the first rate quoted. Several strategies directly reduce your APR—some require time, others just effort.

Improve your credit before applying. Even modest gains pay off. Jumping from 685 to 720 can drop your rate by 2 full percentage points. Prioritize paying credit cards below 30% utilization. Pull your reports from all three bureaus and dispute any errors. Avoid any new credit inquiries for 3-6 months before applying. A 40-point score bump on a $25,000 loan saves roughly $1,200 over five years. That's real money for a few months of financial discipline.

Increase your down payment. Each additional $1,000 down can shave 0.1-0.2 points off your rate while reducing what you're financing. Target 20% if you can swing it. This signals lower risk—you're committed. Sell your current car privately instead of trading it in. Dealers typically offer $1,500-$2,500 below private sale value. That difference funds a bigger down payment.

Shop multiple lenders within two weeks. Credit scoring models treat multiple auto loan inquiries within 14 days as a single inquiry—your score doesn't suffer. Line up quotes from at least one credit union, one traditional bank, and one online lender. Use your lowest offer as leverage. Many lenders will match or beat competitors to earn your business. This isn't theory—I've watched people drop their quoted rate by 1.5 points just by showing a competing offer.

Choose shorter terms if your budget allows. Selecting 48 months instead of 72 typically cuts your rate by 0.5-1.5 percentage points. Yes, monthly payments rise. But you'll pay thousands less in total interest and build equity faster. Calculate both scenarios before deciding which fits your financial situation.

Consider a co-signer with strong credit. If your score sits in subprime territory, adding a co-signer with 750+ credit can qualify you for prime rates—potentially cutting your APR in half. The co-signer assumes equal legal responsibility for the debt. This works best with family who trust your ability to pay. One missed payment damages their credit too.

Plan to refinance after 12-18 months. If your credit improves or market rates drop, refinancing captures better terms. Borrowers who initially accepted subprime rates often successfully refinance into prime territory after a year of on-time payments. Most effective if you avoided extended terms initially—hard to refinance 84-month loans profitably.

Borrowers who actively employ these strategies typically secure rates 2-3 percentage points lower than those accepting the first offer. That compounds to thousands in savings. The average interest rate for used car loan applicants who shop aggressively runs dramatically lower than passive buyers.

Author: Derek Halvorsen;

Source: ruralxchange.net

Frequently Asked Questions About Used Car Loan Rates

The used car lending market rewards preparation more generously than almost any other consumer financing category. Rates swing wildly based on factors mostly within your control—credit score, down payment, lender selection, term length.

Before visiting dealerships, know your credit score. Secure 2-3 pre-approval offers. Calculate what monthly payments fit your budget at different rate levels. This groundwork prevents emotional decisions and high-pressure sales tactics from steering you into unfavorable five-year contracts.

Remember that sticker price tells only part of your total cost story. A $22,000 car financed at 18% APR costs more over five years than a $25,000 car at 7%. Focus on the total amount you'll pay, not just whether the monthly payment fits.

Current lending conditions favor borrowers with good credit and punish those with poor credit more severely than we've seen in years. If your credit needs repair, consider delaying your purchase by 6-12 months while you improve your score. The rate reduction you'll earn often exceeds what you'd save through aggressive price negotiation on the vehicle itself.

Compare aggressively. Question every quote. Don't accept the first offer. Your diligence converts directly into money saved—sometimes thousands of dollars over the loan's life.

Related Stories

Read more

Read more

The content on this website is provided for informational and educational purposes only. It offers general guidance on topics related to car loans, auto refinancing, interest rates, credit scores, loan terms, and vehicle financing options. The information presented should not be considered financial, legal, or professional advice.

Auto loan terms, interest rates, approval requirements, and refinancing options may vary depending on the lender, credit profile, and individual circumstances.

While we aim to keep the information accurate and up to date, we make no guarantees regarding its completeness or reliability. Visitors should review official loan documents and consult with qualified financial professionals before making decisions related to auto loans or refinancing.