Journal About Car Loan Guide

Source: ruralxchange.net

Welcome to Car Loan Guide — a resource designed to explain auto loans and vehicle financing in a clear and practical way. Our goal is to help readers understand how car loans work, how interest rates are calculated, and how different financing options can affect the cost of buying or refinancing a vehicle.

In our journal, we publish guides covering topics such as refinancing a car loan, car loan rates by credit score, pre-approved auto loans, credit union financing, and car loans for people with bad or no credit. We also explain important lending concepts including APR, loan terms, down payments, approval requirements, and prequalification.

Our articles explore common situations related to auto financing, including negative equity, trading in a car with a loan, removing a cosigner, paying off a car loan early, and managing monthly payments. We also explain how loan conditions may vary between lenders and how different credit profiles can affect approval and interest rates.

Read more

Top Stories

Read more

Read more

Read more

Read more

Trending

Read more

Read more

Latest articles

Most read

Read more

Read more

In depth

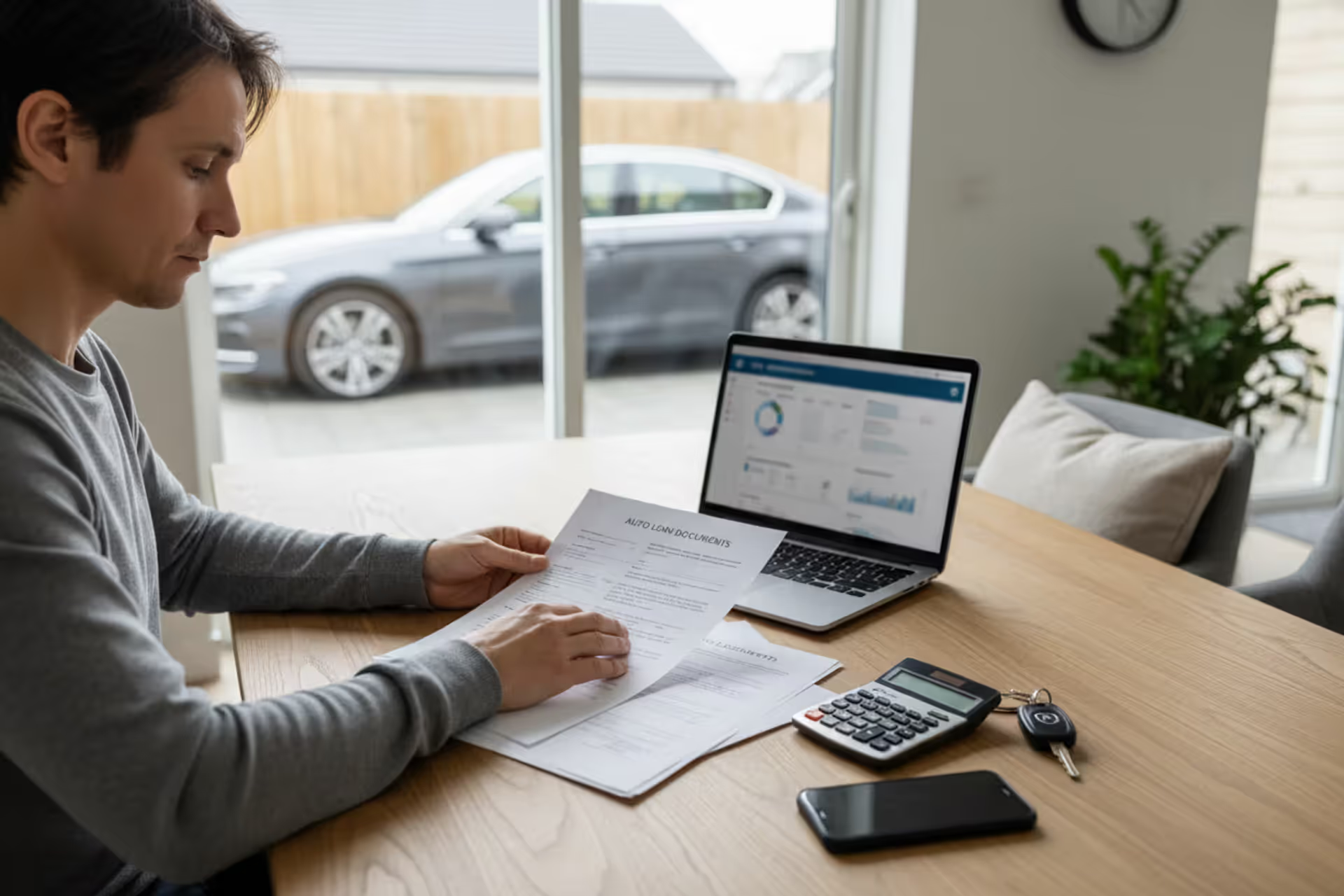

Yes, you can refinance a car loan—and millions of borrowers do it every year to save money, adjust their monthly budget, or change loan terms. Refinancing replaces your existing auto loan with a new one, ideally with better terms that fit your current financial situation. Whether you've improved your credit score, interest rates have dropped, or your income has changed, refinancing offers a way to renegotiate the deal you originally signed.

Understanding when and how to refinance can mean the difference between saving thousands of dollars over the life of your loan or wasting money on unnecessary fees. This guide breaks down everything you need to know about car loan refinancing, from eligibility requirements to step-by-step instructions.

What Car Loan Refinancing Means

When you refinance a car loan, you're essentially taking out a new loan to pay off your existing one. The new lender pays your current lender the remaining balance, and you begin making payments under the new loan's terms—which might include a different interest rate, monthly payment, or loan duration.

People typically consider refinancing when they spot an opportunity to improve their loan terms. Maybe you financed through the dealership at a higher rate because you needed the car immediately. Perhaps your credit score has jumped 80 points since you bought the vehicle. Or interest rates across the market have dropped since you signed your original paperwork.

The basic process involves applying with a new lender, g...

Read more

The content on this website is provided for informational and educational purposes only. It offers general guidance on topics related to car loans, auto refinancing, interest rates, credit scores, loan terms, and vehicle financing options. The information presented should not be considered financial, legal, or professional advice.

Auto loan terms, interest rates, approval requirements, and refinancing options may vary depending on the lender, credit profile, and individual circumstances.

While we aim to keep the information accurate and up to date, we make no guarantees regarding its completeness or reliability. Visitors should review official loan documents and consult with qualified financial professionals before making decisions related to auto loans or refinancing.