Person reviewing auto loan refinance options at home with laptop and smartphone

How to Refinance Car Loan Credit Union Options

That monthly car payment hitting your checking account? It doesn't need to stay locked at whatever rate the dealer gave you two years ago. Plenty of drivers drop their payments anywhere from $50 to over $150 by moving their loan to a credit union—especially if they originally financed through a dealership at some ridiculous rate.

Credit unions operate under fundamentally different rules than regular banks. They answer to members, not investors chasing quarterly profit targets. That structure lets them charge less for loans and skip a lot of the junk fees that banks love to tuck into the fine print. You'll typically find their rates sitting 1–2 percentage points below what places like Chase or Bank of America advertise, and on a four or five-year loan, that gap translates to real money.

The membership requirement trips people up, though. You can't just walk in off the street like at a regular bank. Each credit union has specific rules about who qualifies to join, and their application processes work differently than what you're used to. We'll cover the membership hoops, what paperwork they actually need, and how to figure out if refinancing will actually put money back in your pocket.

Why Refinance Your Car Loan with a Credit Union

Credit unions think about loan pricing completely backwards from traditional banks. No shareholders breathing down their necks means they can function on slimmer margins without Wall Street having a meltdown.

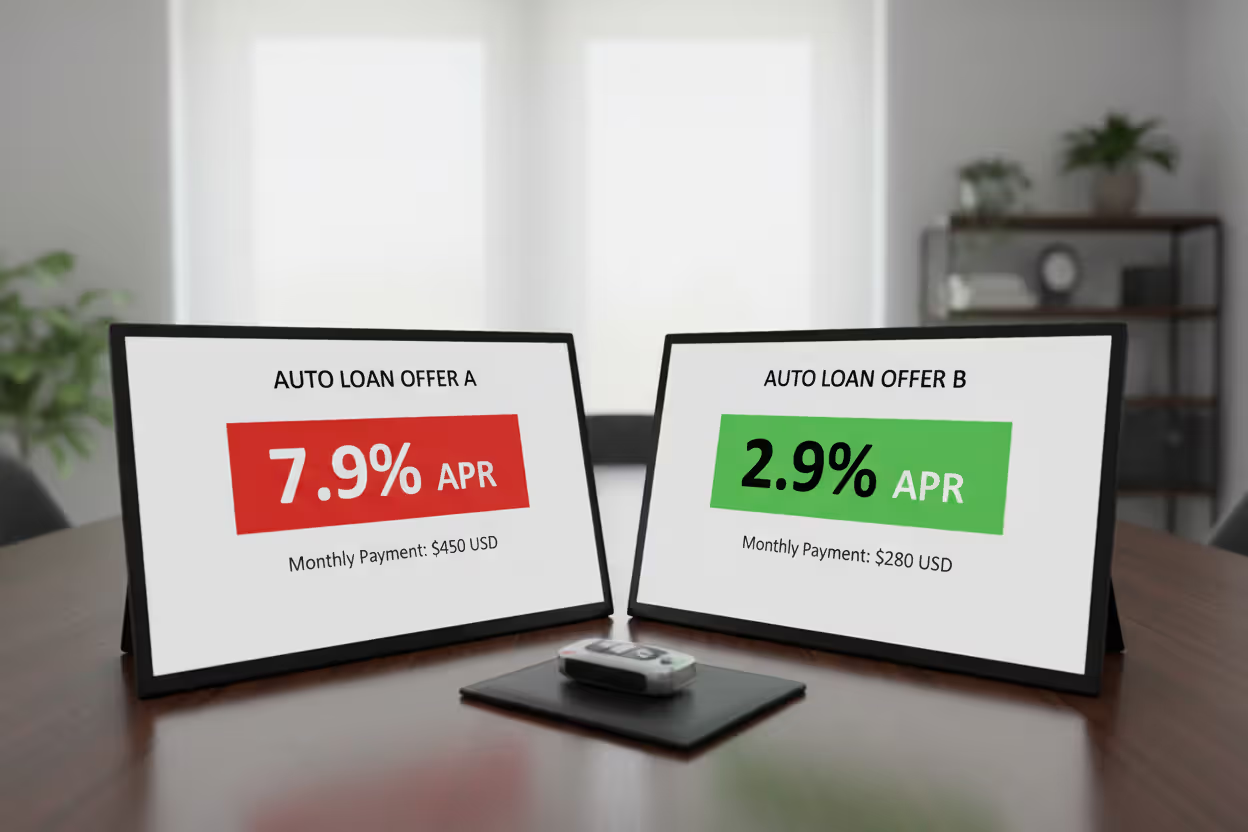

The rate differences become obvious fast once you start comparing actual numbers. Looking at current 2026 rates, someone with a 680 credit score might see 5.2% APR at a credit union while the bank across the street quotes 6.8%. Run those numbers on a $25,000 loan with four years remaining, and that 1.6-point gap saves you close to $950 in interest charges. Not retirement money, but enough to matter.

Author: Samantha Whitaker;

Source: ruralxchange.net

How they treat you changes the whole experience. Credit union loan officers can actually make judgment calls instead of just feeding your info into an algorithm. Say your score dropped to 640 after a three-month unemployment stretch last year, but you've been back at work for six months with solid income. A credit union underwriter will read your explanation and consider your full situation. Bank computers just see the dip and auto-decline you.

Loan terms extend to vehicles most banks won't touch anymore. Lots of credit unions will refinance cars pushing 150,000 miles or models from 2015. Banks usually cut you off at 100,000 miles and seven or eight years old because their risk models show older vehicles default more. Credit unions don't automatically write off older cars—they just price the rate slightly higher to cover the added risk.

Some even offer skip-a-payment features once a year if money gets tight. Interest keeps running that month, so you're not getting a freebie, but it beats a 30-day-late mark on your credit report when unexpected bills pile up.

Fee schedules stay cleaner. Application charges? Usually nothing. Prepayment penalties if you pay off the loan early? Most credit unions ditched those ages ago. Banks routinely bury $100–$300 origination fees into your total loan amount, quietly inflating what you actually owe.

The tradeoff: you need to qualify for membership first. Could be living in certain counties, working for specific employers, or joining some affiliated nonprofit. Membership usually costs $5–$25, though that money just sits in a savings account you can pull from whenever.

Credit Union Car Loan Refinance Eligibility Requirements

The approval process isn't nearly as exclusive as it sounds, but every credit union draws different boundaries around who gets in.

Membership Qualifications

Each institution operates under "field of membership" rules that define their boundaries. Ways you might qualify:

- Geographic ties: Living, working, or owning property in specific zip codes or counties they serve

- Employment links: Current or former employees of companies they partner with—government offices, school systems, hospitals, corporations

- Group affiliations: Members of partner organizations like churches, alumni associations, professional groups

- Family connections: Immediate relatives of existing members (spouses, parents, siblings, kids)

Some cast their nets pretty wide. Navy Federal requires military connections, but that includes veterans, active military, reservists, plus all their family members. PenFed lets anyone join if they become a member of the National Military Family Association for $17—pay that once and you're in permanently.

Call their membership department before filling out loan applications. The qualification process usually takes 10–15 minutes and means opening a basic savings account with $5–$25.

Author: Samantha Whitaker;

Source: ruralxchange.net

Credit Score and Income Criteria

Credit unions will work with scores as low as 580, though your rate improves dramatically once you cross 660. Standard expectations look like:

- Credit score: 580 gets you in the door; 700+ unlocks their best pricing

- Debt-to-income ratio: Under 45% including your new car payment

- Loan-to-value ratio: Below 125% (you can't owe more than 25% above what the car's worth)

- Income proof: Recent pay stubs if you're a W-2 employee; tax returns if you're self-employed

Can I refinance my car loan with a credit union after my credit has improved? This scenario actually represents one of the smartest times to refinance. Maybe you bought your car two years back with a 620 score and dealer financing stuck you at 12% APR. Your score's climbed to 720 since then because you've been making every payment on time. You could potentially knock that rate down to 5–6%, slashing your interest costs by more than half.

Credit unions will refinance loans from anywhere—banks, captive finance companies like Honda Financial, even other credit unions. Your original lender can't lock you in.

How the Credit Union Refinance Process Works

Author: Samantha Whitaker;

Source: ruralxchange.net

Budget 5–10 business days from application to getting funded. Here's the typical sequence:

Step 1: Get your membership squared away if you're not already a member. Fill out their online or in-branch application and make the initial deposit. Some credit unions approve instantly; others need 1–2 business days.

Step 2: Pull together your paperwork before touching the loan application. You'll need your current payoff statement showing the account number, recent pay stubs or tax returns, insurance declarations page proving you carry comprehensive and collision coverage, and vehicle information (VIN, make, model, year, current mileage).

Step 3: Submit the refinance application through their website, mobile app, or at a branch. Most give you a preliminary decision right away, though final approval waits while they verify documents. Figure 15–20 minutes for the application itself.

Step 4: They'll value your vehicle without you lifting a finger. Unlike when you're buying a car and they might send someone to physically inspect it, refinances lean on NADA, Kelley Blue Book, or Edmunds data. They punch in your VIN and odometer reading to estimate what it's worth today. If you owe more than 125% of that number, you'll either pay down the gap or potentially need additional collateral.

Step 5: Review loan documents electronically or in person once approved. Focus on the APR, not just what your monthly payment becomes—stretching your term lowers the payment but might cost you more in total interest. Verify there's no prepayment penalty if you think you'll pay extra or refinance again down the road.

Step 6: Payoff and title transfer happen at the same time. The credit union wires money directly to your current lender and handles the paperwork to switch the lien over to themselves. Keep paying your old lender until they confirm receiving the payoff, which typically takes 5–10 business days. Your first credit union payment usually isn't due for 45 days.

Watch this: some people leave autopay running to their old lender even after the credit union sends the payoff money. Always confirm with your original lender that they received full payment before you cancel those automatic payments.

Comparing Credit Union vs Bank Refinance Rates

Rate gaps between different lender types show you exactly where the best deals hide.

| Feature | Credit Union | Bank | Online Lender |

| Typical APR Range | 5.2%–7.8% | 6.8%–9.5% | 5.8%–10.2% |

| Must Join First | Yes | No | No |

| Days to Close | 5–10 business days | 7–14 business days | 3–7 business days |

| Typical Fees | $0–$50 | $100–$300 | $0–$150 |

| Service Options | In-person + phone | In-person + phone | Phone/chat only |

| Available Terms | 24–84 months | 36–72 months | 24–72 months |

Real borrower examples show what this means for your wallet. Let's say you've got a 680 credit score with $20,000 left on your loan and 48 months to go:

- Your current rate (original dealer financing): 9.5% APR = $498 monthly, $3,904 total interest

- Credit union refinance rate: 5.8% APR = $469 monthly, $2,512 total interest

- What you gain: $29 less each month, $1,392 less in interest over the full term

If that credit union charges a $75 processing fee, you'd make it back in under three months through lower payments.The math favors credit union refinancing when you can drop your rate by at least a full percentage point and you're planning to keep that vehicle for at least two more years. Interest savings compound over time, and most borrowers don't realize how much they're hemorrhaging to interest with their current arrangements

— Jennifer Martinez

Common Mistakes When Refinancing with Credit Unions

Even straightforward refinances blow up without proper planning. These mistakes happen constantly:

Timing it wrong destroys your potential gains. Refinancing during months 1–12 of your original loan rarely pays off because you've barely chipped away at the principal—those early payments flow almost entirely to interest, so your balance stays high while the car has already lost 20–30% of its value. Flip side: waiting until just 12–18 months remain offers minimal benefit since you've already paid most of the interest.

Sweet spot: 12–36 months into a 60–72 month loan, once you've built some equity but still face substantial interest charges ahead.

Author: Samantha Whitaker;

Source: ruralxchange.net

Checking just one credit union leaves money on the table. The first place you contact might not offer the best rate. Apply to 2–3 different credit unions within a two-week window. Credit scoring systems treat multiple auto loan inquiries during a 14-day span as a single event, so you won't see cascading damage to your score.

Fixating on monthly payments hides the real costs. A $50 lower payment looks fantastic until you realize they achieved it by stretching your 48-month loan out to 60 months. Your payment dropped, sure, but you'll bleed more total interest. Always compare APRs and total interest across the complete loan term, not just the monthly hit to your checking account.

Refinancing underwater loans without grasping the risk: Owing $18,000 on a car worth $14,000 puts you $4,000 upside down. Some credit unions will refinance at 125% LTV, but you're essentially borrowing against a depreciating asset. If someone totals your car next month, insurance cuts a check for the $14,000 actual cash value, leaving you personally on the hook for that $4,000 gap unless you maintain gap insurance coverage.

Missing prepayment penalties on your existing loan: Check your current loan paperwork before applying anywhere. Some lenders hit you with $100–$500 for early payoff, which could wipe out your entire refinancing benefit.

Letting insurance coverage lapse during the switch: Keep continuous coverage throughout your refinance. The new lender won't fund the loan without proof of insurance, and any gap in coverage could trigger default provisions in your loan contract.

How Much You Can Save Refinancing Through a Credit Union

What you'll actually save depends on your current rate, what you still owe, and what rate you can lock in now. Here are three realistic 2026 examples:

Scenario 1: Breaking free from expensive dealer financing - Original loan: $30,000 at 11.9% APR for 72 months - Balance after 8 months: $28,200 - Credit union refinance: 6.2% APR for 64 months - Monthly payment shift: $515 (down from $568) - Total interest you avoid: $4,890

Scenario 2: Capitalizing on improved credit halfway through - Original loan: $22,000 at 8.5% APR for 60 months - Balance after 24 months: $14,800 - Credit union refinance: 5.5% APR for 36 months - Monthly payment shift: $448 (down from $453) - Total interest you avoid: $890

Scenario 3: Small improvement on an already decent rate - Original loan: $18,000 at 6.8% APR for 60 months - Balance after 18 months: $12,900 - Credit union refinance: 5.1% APR for 42 months - Monthly payment shift: $318 (down from $356) - Total interest you avoid: $520

When fees factor in, calculate your break-even point. Take whatever fees they charge and divide by your monthly savings to see how many months you need to keep the new loan to come out ahead. Pay $100 in fees while saving $40 monthly? You break even after 2.5 months—everything after that is pure profit.

Author: Samantha Whitaker;

Source: ruralxchange.net

Most credit unions post calculators on their websites where you plug in your current loan details and instantly see projected savings. These tools answer whether refinancing makes financial sense before you spend time on applications.

Frequently Asked Questions

Transferring your auto loan to a credit union produces measurable financial benefits for borrowers meeting membership criteria. Lower rates, personalized service, and flexible underwriting combine to reduce monthly payments and total interest charges—often by hundreds or thousands of dollars.

Success requires understanding membership pathways, assembling proper documentation, and comparing offers from multiple credit unions within a compressed timeframe. Avoid common mistakes like refinancing too early, unnecessarily extending your loan term, or ignoring fees that erode your net benefit.

The strongest refinance candidates have improved their credit since originally financing, currently carry rates above 7%, and plan to keep their vehicles for at least two more years. Even a 1–2 point rate reduction generates meaningful savings over the remaining loan term.

Start by identifying 2–3 credit unions where you qualify for membership, review current refinance rates on their websites, and use their calculators to estimate your potential benefit. The application process consumes less than an hour, and the long-term financial impact justifies the effort for most borrowers paying above-market rates.

Related Stories

Read more

Read more

The content on this website is provided for informational and educational purposes only. It offers general guidance on topics related to car loans, auto refinancing, interest rates, credit scores, loan terms, and vehicle financing options. The information presented should not be considered financial, legal, or professional advice.

Auto loan terms, interest rates, approval requirements, and refinancing options may vary depending on the lender, credit profile, and individual circumstances.

While we aim to keep the information accurate and up to date, we make no guarantees regarding its completeness or reliability. Visitors should review official loan documents and consult with qualified financial professionals before making decisions related to auto loans or refinancing.